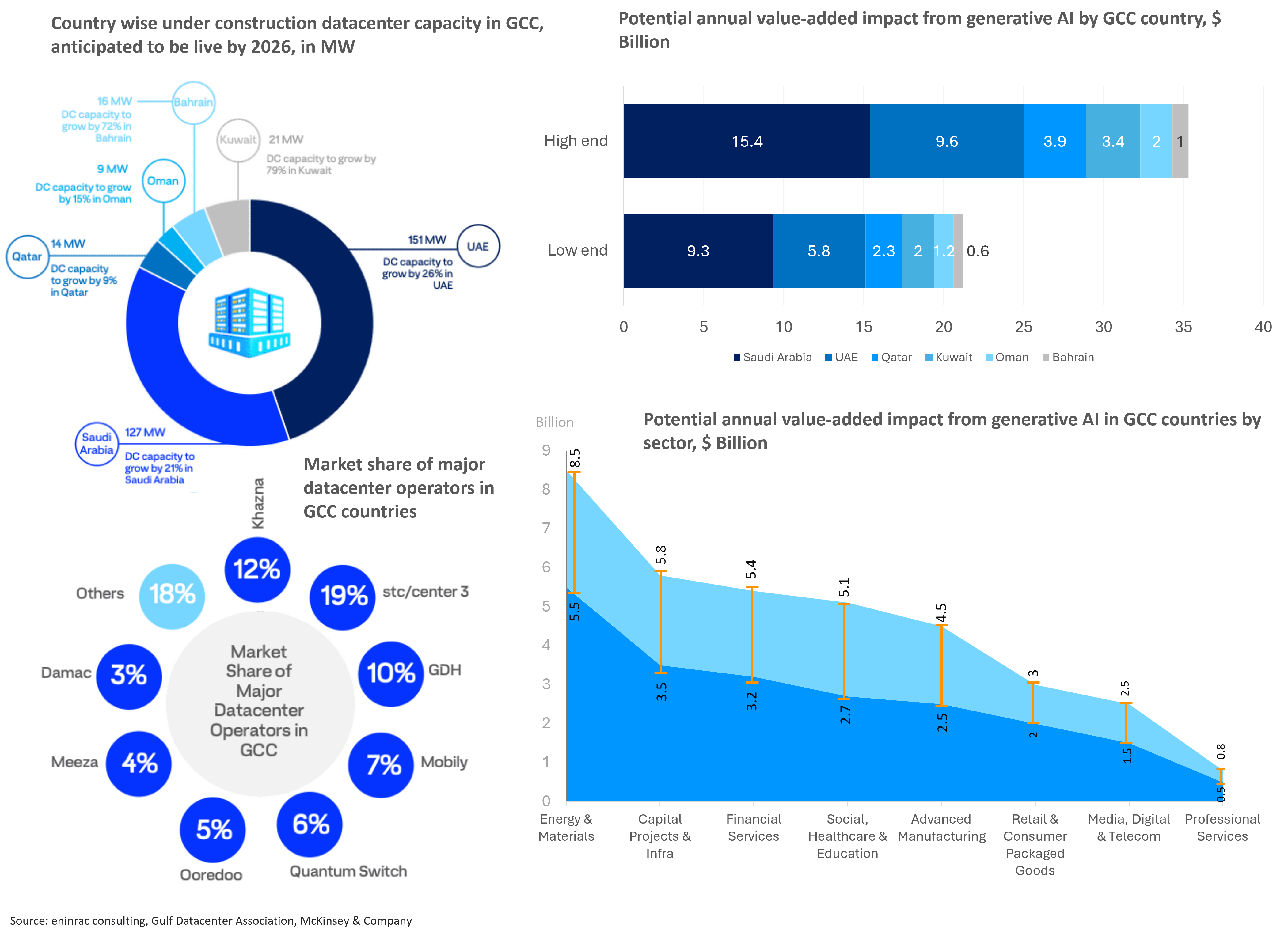

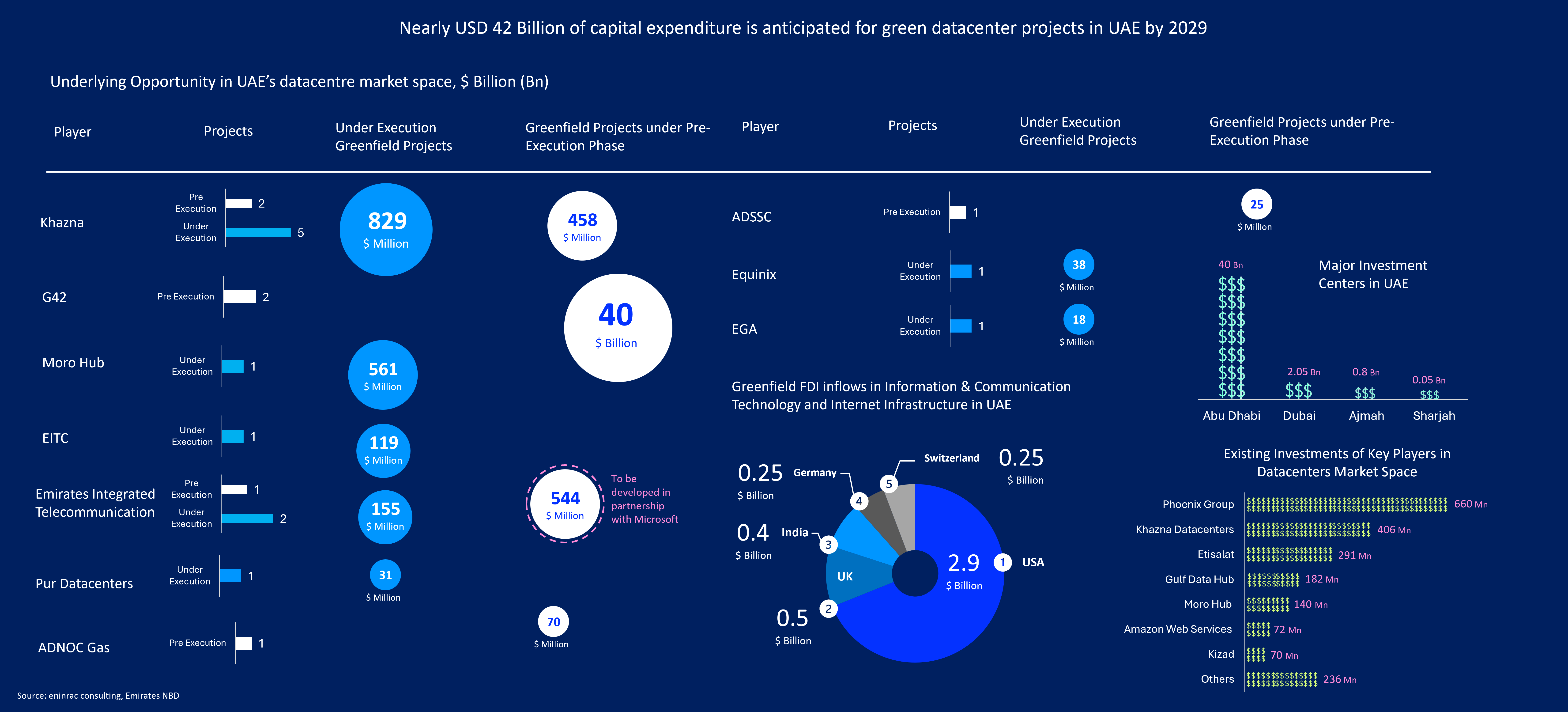

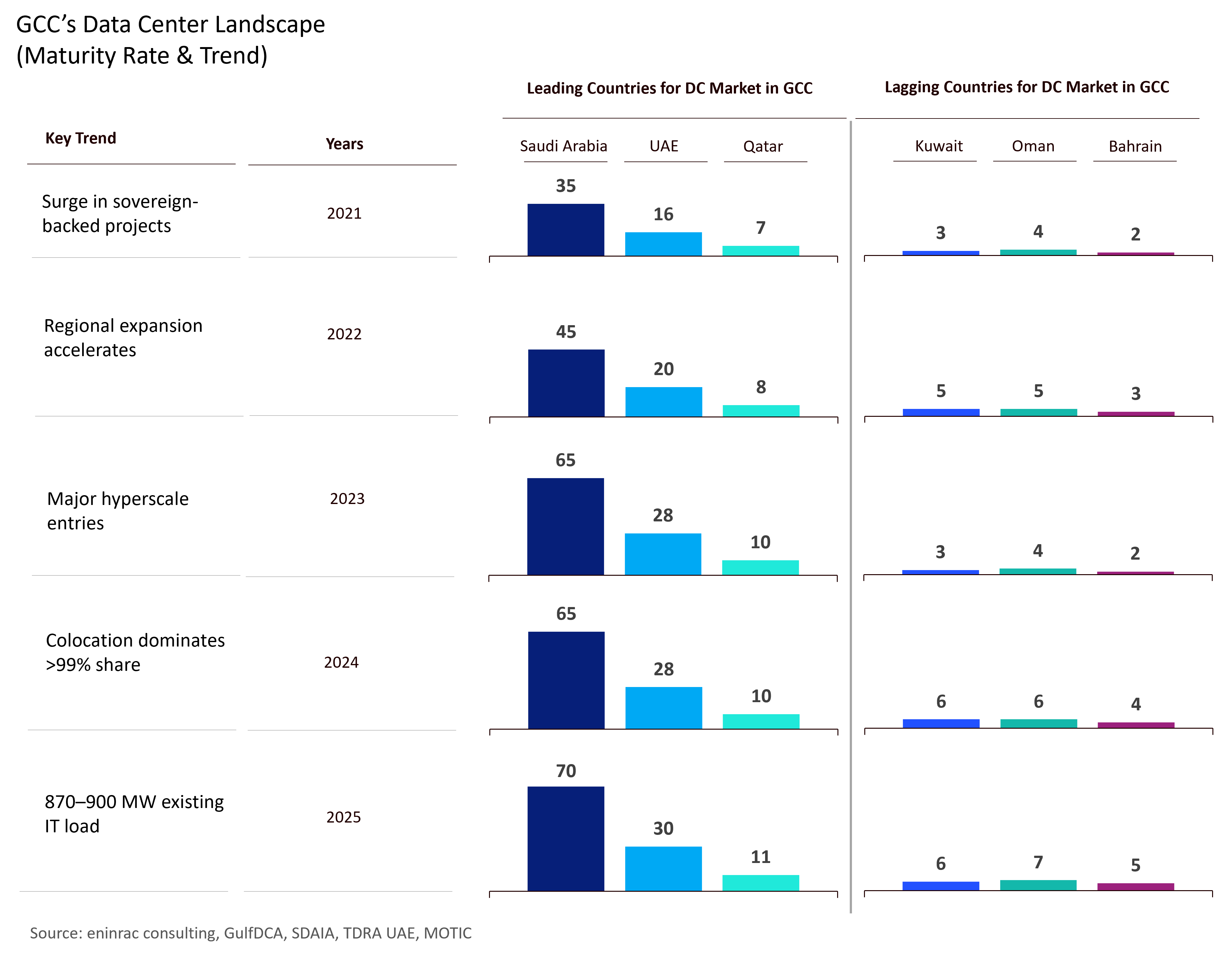

The GCC data center ecosystem has entered a phase of accelerated maturity. As of 2025, the region hosts an estimated 129 operational facilities with an aggregate IT load between 870–900 MW. Saudi Arabia and the UAE account for over two-thirds of this capacity, driven by hyperscale and sovereign digital infrastructure investments. An additional 4,000 MW of capacity is under development between 2024 and 2028, positioning the GCC as one of the fastest-growing data center hubs globally. Annual CapEx investment is projected at USD 3.1 billion, focused on civil works, power systems, and MEP infrastructure. Khazna Data Centers (UAE) remains the dominant player, holding approximately 70 percent market share across operating and under-construction capacity. The market remains predominantly colocation-led, though hyperscale and edge facilities are set to expand their footprint over the next decade.

IT Load Growth Trend (2018–2030): Scaling for Digital Sovereignty

The GCC and wider Middle East data center capacity has grown nearly 3.5 times between 2018 and 2025, propelled by rising hyperscale demand, cloud localization mandates, and enterprise digitization. IT load across the Middle East increased from ~330 MW in 2018 to ~900 MW in 2025, with projections crossing 1,300 MW by 2030. This capacity expansion reflects a clear regional intent to build sovereign digital ecosystems capable of supporting artificial intelligence, IoT networks, and data-intensive applications. The largest share of this incremental load is being absorbed by hyperscale data centers and government-backed digital infrastructure programs.

Facility Type Evolution: Transitioning Beyond Colocation Dominance

While colocation remains the backbone of GCC data infrastructure with over 99 percent share in 2024, market dynamics are gradually shifting. The rise of hyperscale facilities (5–7 percent projected by 2030) signals the maturing of cloud-native demand and digital transformation initiatives. Simultaneously, edge computing is gaining ground, expected to reach 7–10 percent of facilities by 2030. Edge deployments will be driven by smart city programs, 5G rollouts, and AI-enabled low-latency applications across logistics, energy, and fintech sectors. This evolution marks a structural decentralization of data infrastructure, where hyperscale and edge nodes complement the colocation base, enabling both national data sovereignty and operational resilience.

Datacentres are recognized as critical national infrastructure across GCC nations and receive strong policy-level support. In a notable recent development, Saudi Arabia unveiled Project Transcendence, a US $100 billion AI initiative aimed at positioning the Kingdom as a global leader in advanced digital capabilities. The sector is also benefiting from substantial investment in enabling infrastructure, especially connectivity. An expanding subsea cable network continues to strengthen the region’s strategic advantage as a digital bridge linking Asia, Europe, and the United States. Across the GCC, governments are competing to accelerate digital transformation and establish themselves as regional and global hubs for AI. Key drivers to the growth of datacentre market across the GCC countries