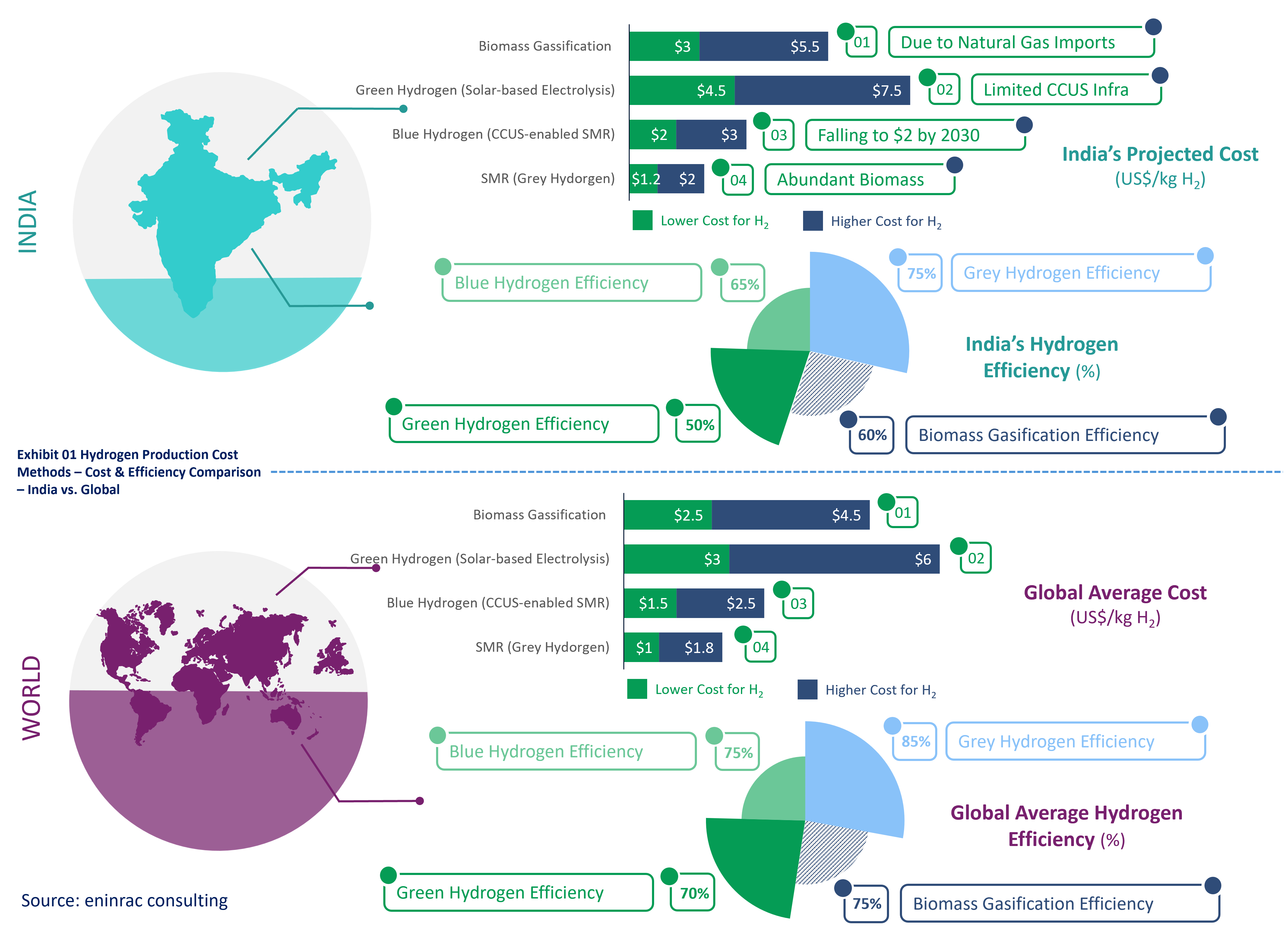

Hydrogen production costs and efficiencies vary widely by method and geography. In India, reliance on imported natural gas raises the cost of grey and blue hydrogen compared to global averages. While green hydrogen remains costlier today, aggressive renewables expansion and policy support are expected to bring costs down to ~$2/kg by 2030. Biomass gasification, leveraging India’s agricultural residue, offers a promising decentralized route. This comparative analysis highlights how India’s hydrogen strategy must balance technology maturity, feedstock availability, and infrastructure readiness to realize its green hydrogen ambitions.

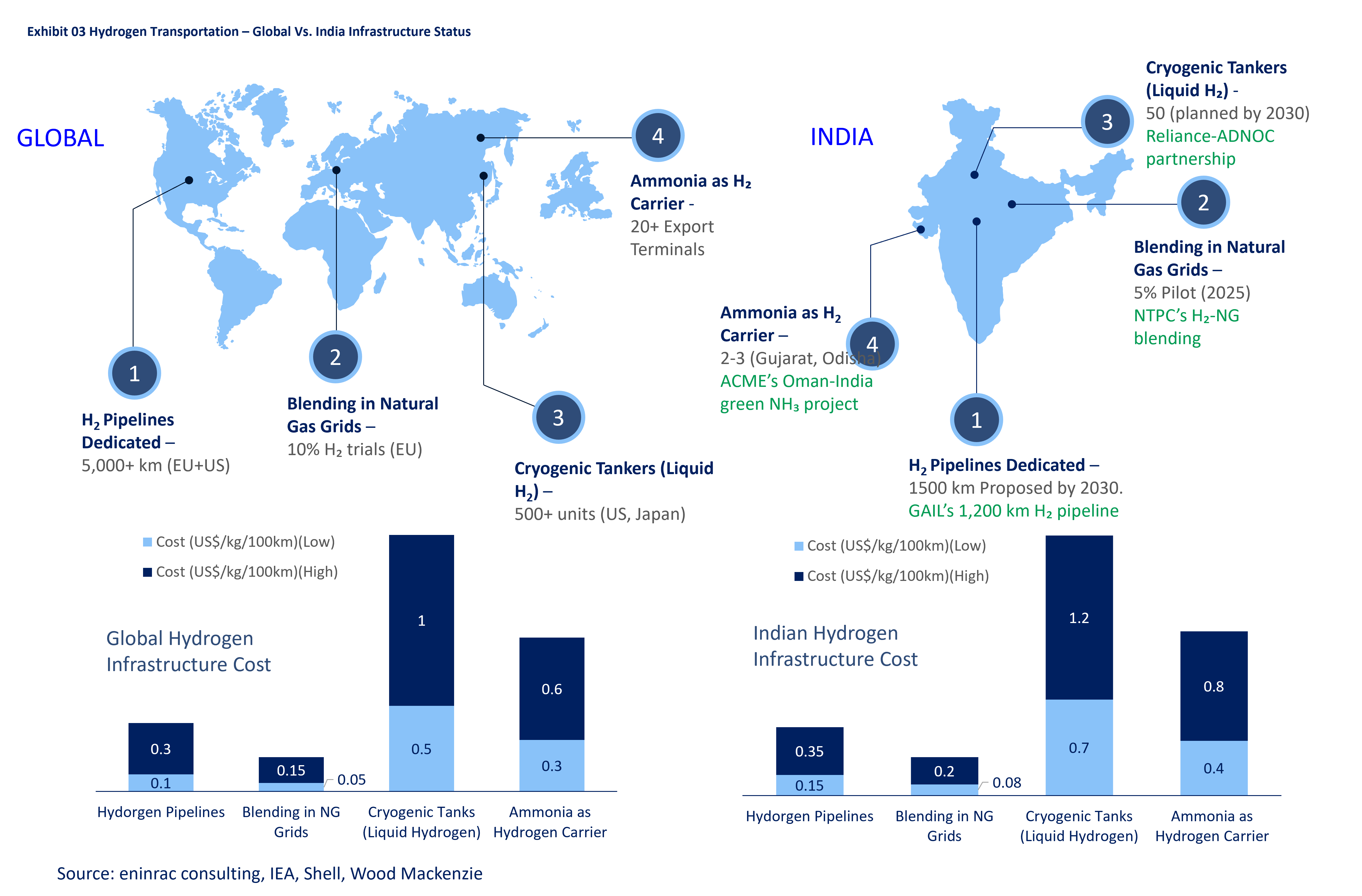

Further, aligning cost competitiveness with global benchmarks is essential for India to emerge as a key hydrogen exporter. Electrolyzer localization, viability gap funding, and scale-driven cost reductions will be crucial. Strategic production clusters near RE zones, ports, and industrial hubs can enhance economics. Policy clarity and cross-sectoral coordination will determine India’s pace in capturing its share of the $100B+ global green hydrogen trade opportunity. Moreover, regional production incentives, carbon pricing mechanisms, and renewable energy banking policies will shape investor confidence. India's ability to integrate hydrogen into refining, fertilizer, steel, and mobility sectors will directly influence demand scaling. The convergence of public-private capital, innovation ecosystems, and strategic international partnerships will define India’s leadership in the hydrogen economy.

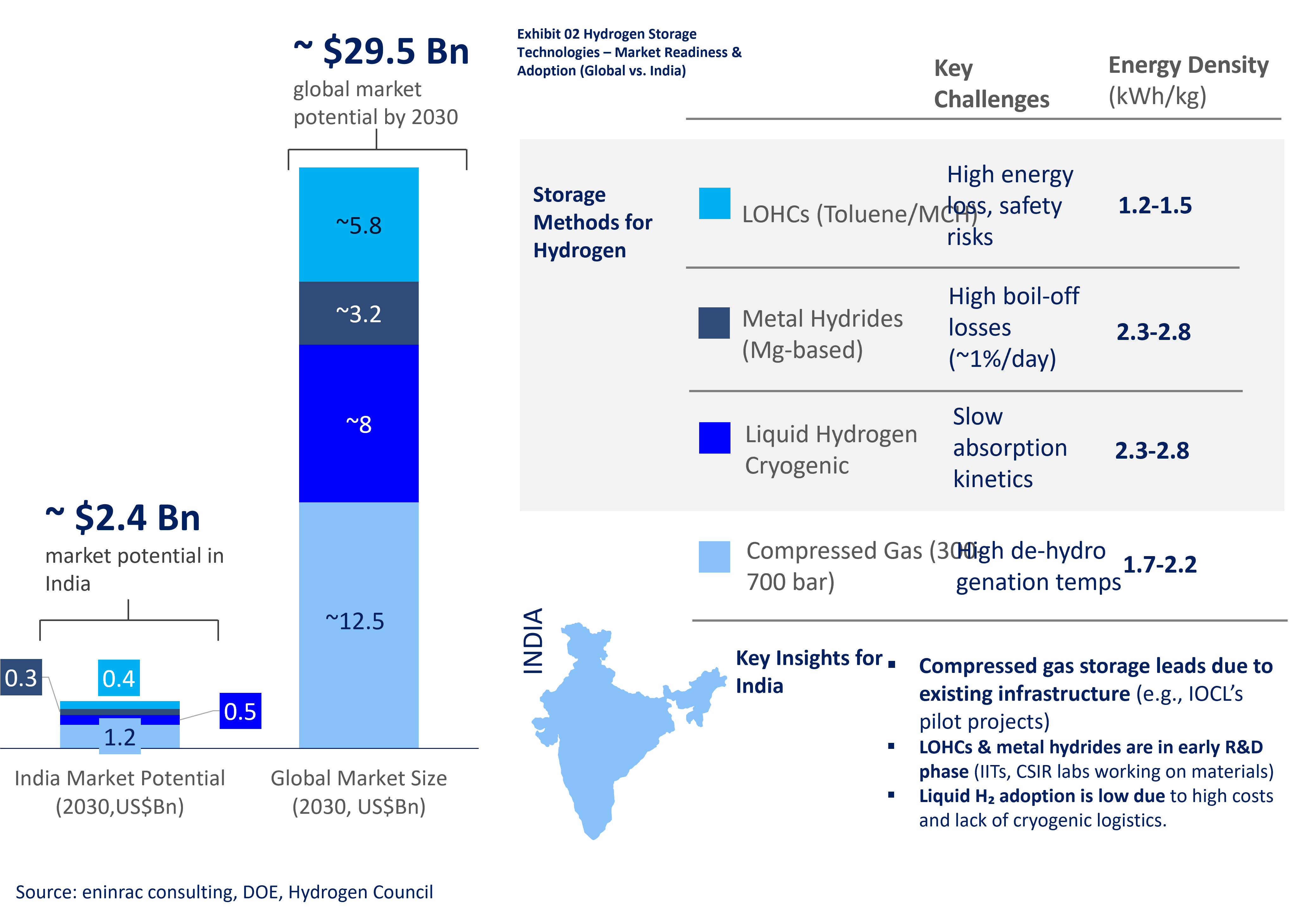

Hydrogen storage remains a critical enabler for realizing the hydrogen economy—impacting transport, distribution, and end-use efficiency. As per Eninrac’s market intelligence, the global hydrogen storage market is poised to cross $30 billion by 2030, with India contributing an estimated $2.4 billion, led by compressed gas and emerging cryogenic solutions.

Compressed hydrogen gas storage (350–700 bar) continues to dominate early deployments, but its low energy density (1.2–1.5 kWh/kg) and energy-intensive compression present safety and cost trade-offs. India’s share in this segment is projected at $1.2 billion, driven by mobility and backup power applications. However, advanced Type IV tank materials and improved valve technologies remain critical to cost optimization. In parallel, liquid hydrogen (LH2) offers higher energy density (2.3–2.8 kWh/kg), yet faces challenges of ~1% daily boil-off losses, impacting viability in long-haul and maritime use cases.

Eninrac analysts note India’s LH2 potential at $0.5 billion, backed by ISRO’s legacy and recent public-private interest. Metal hydrides (e.g., MgH₂) and Liquid Organic Hydrogen Carriers (LOHCs) are gaining traction in R&D and pilot phases. While their energy densities range from 1.5 to 2.2 kWh/kg, their limitations—such as slow kinetics for hydrides and high regeneration temperatures for LOHCs—require further breakthroughs.