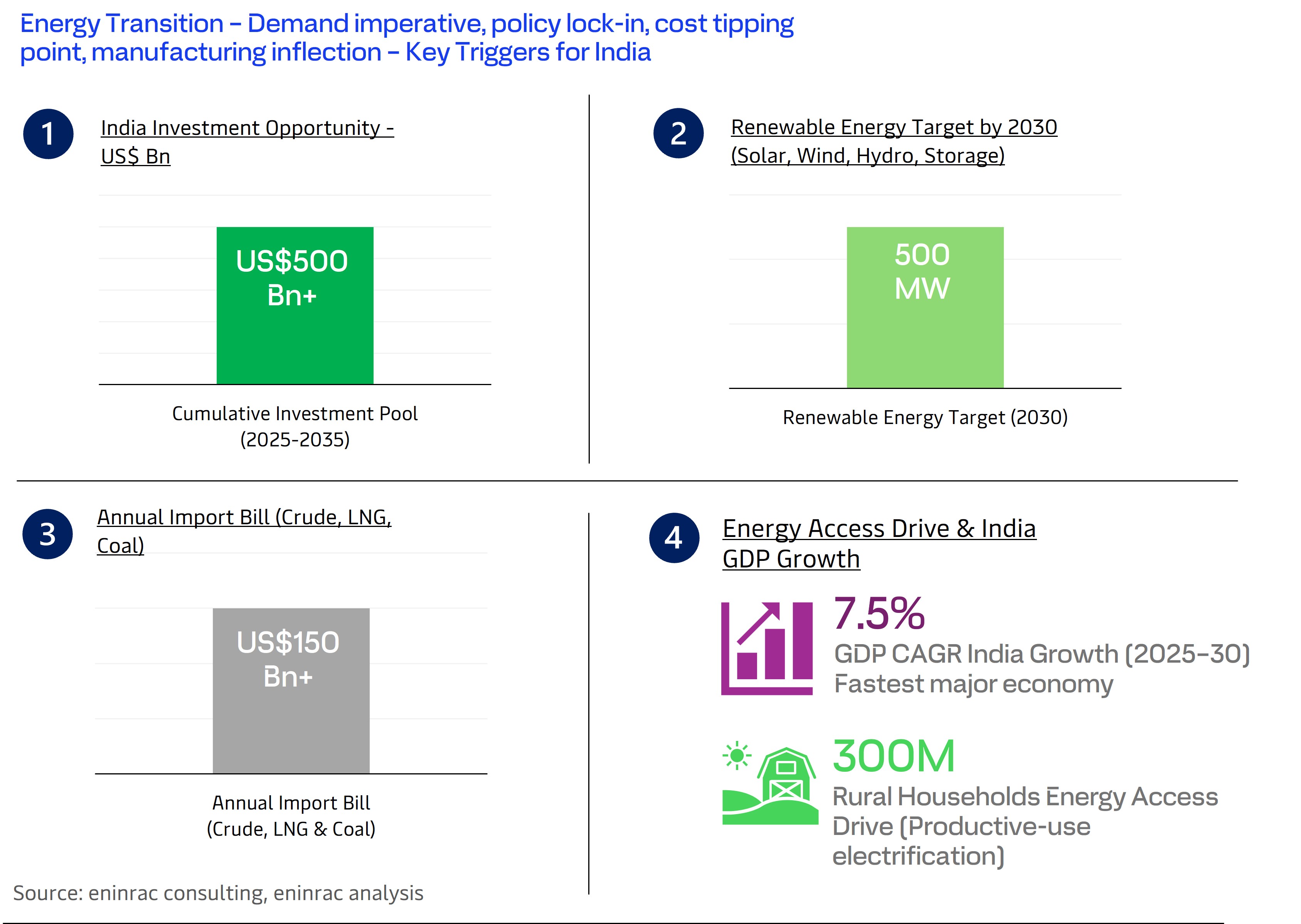

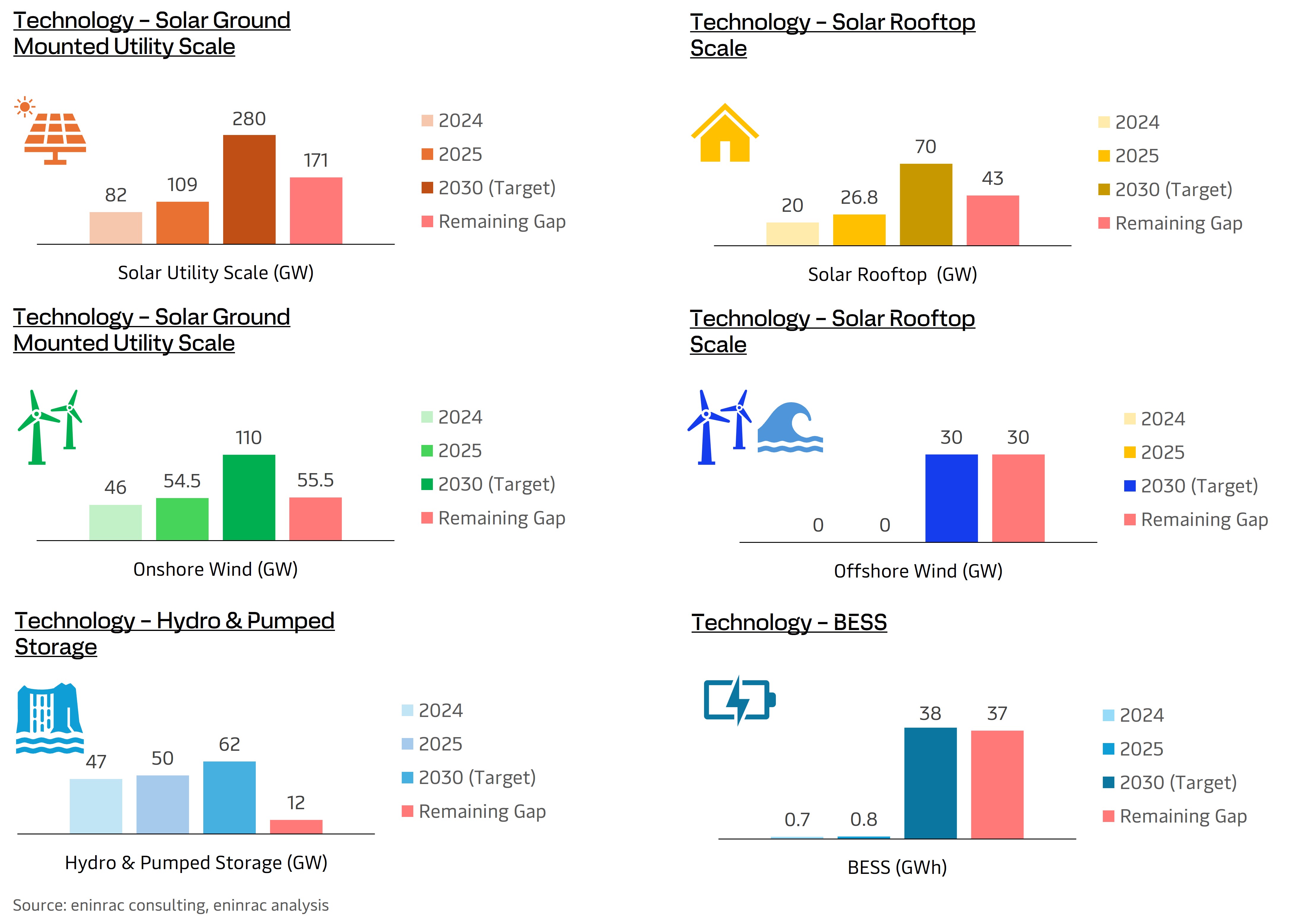

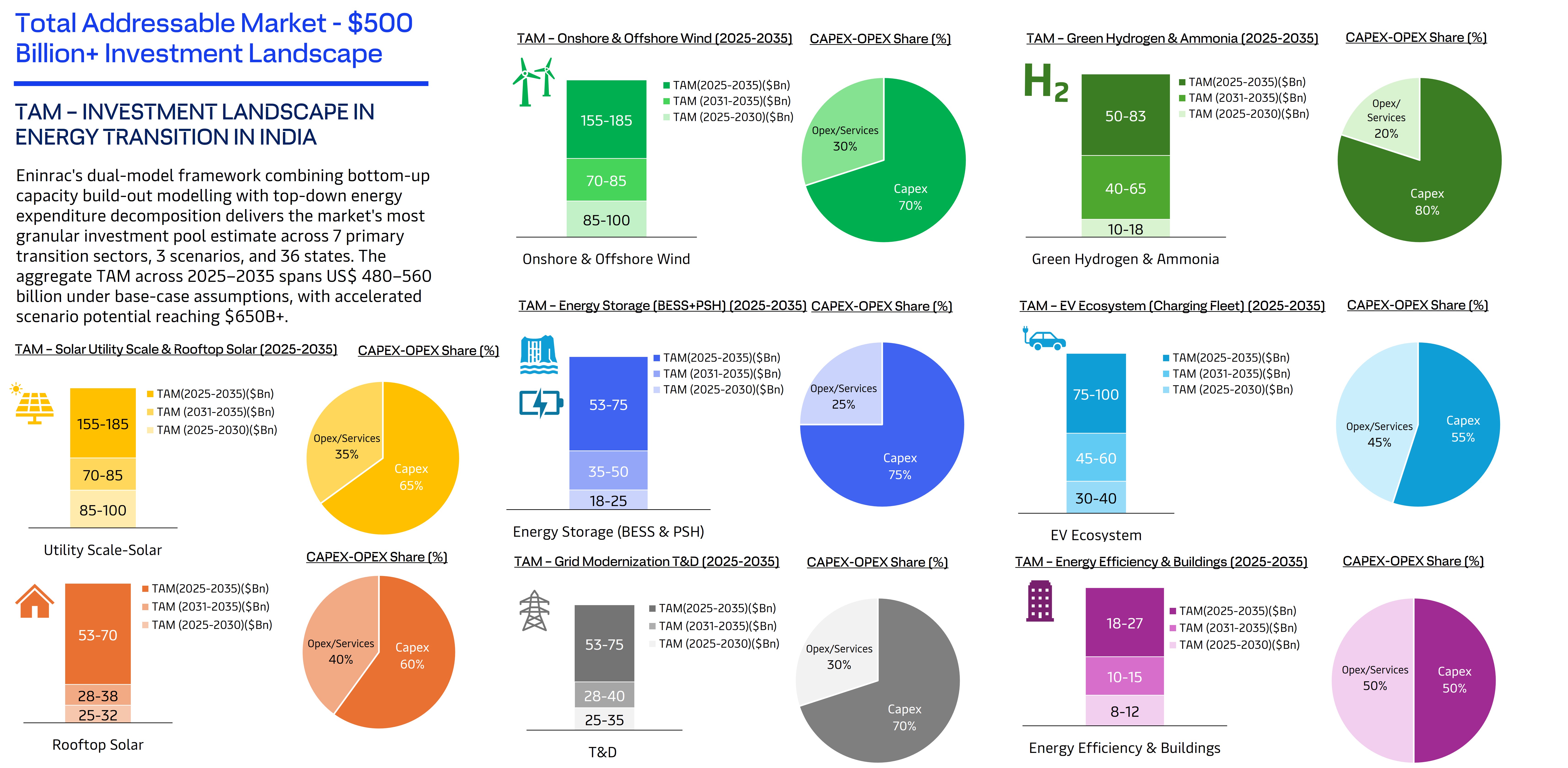

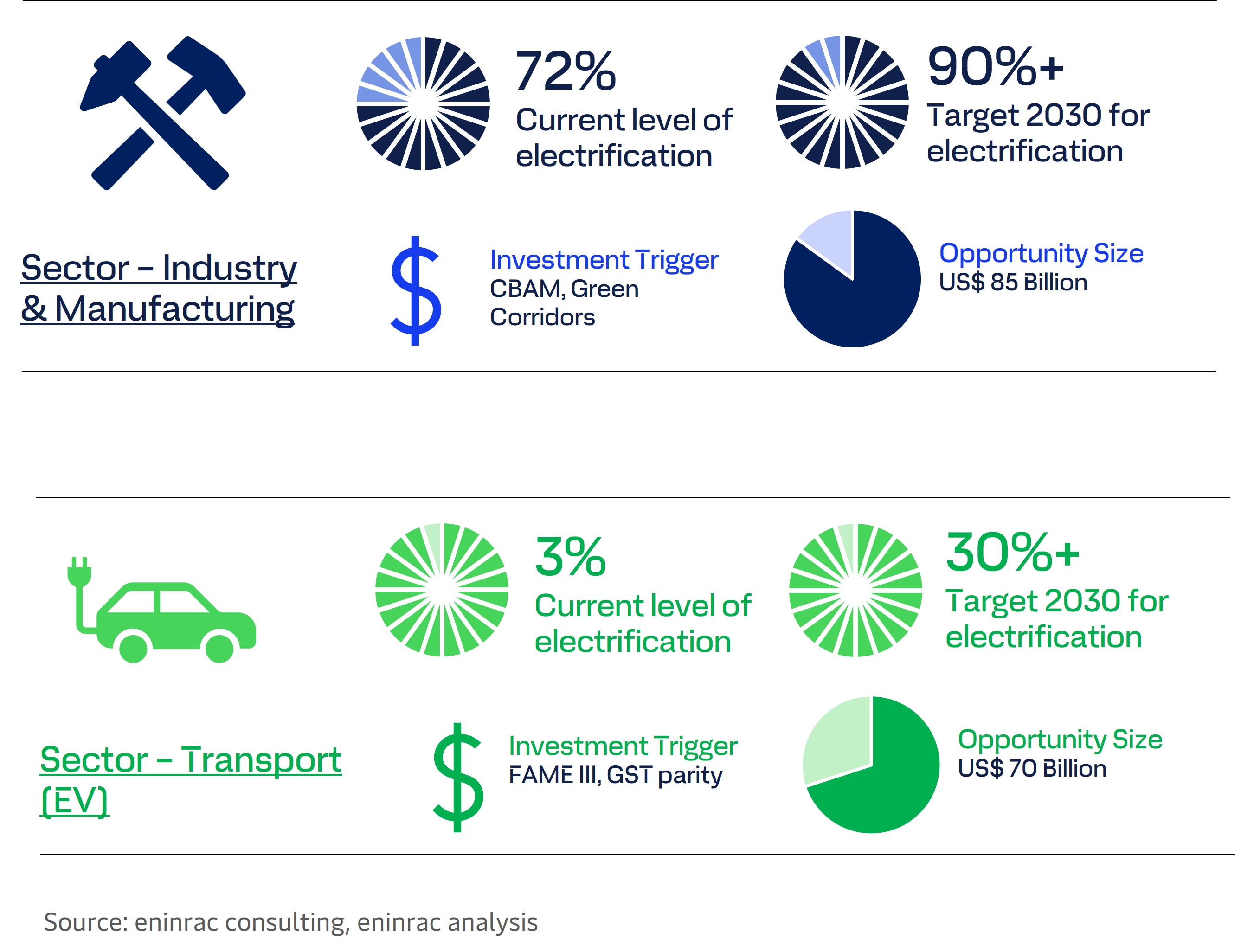

India’s clean‑energy transition is quantified as a $480 bn‑$560 bn investment pool for 2025‑2035, with an upside beyond $650 bn if policy and market dynamics accelerate. To hit the 500 GW non‑fossil target by 2030, the country must add about 295 GW of capacity—roughly 33 GW of utility‑scale solar, 8 GW of rooftop solar and 5‑6 GW of wind each year—a deployment speed never before achieved in India. The total addressable market (TAM) splits into $155‑$185 bn for utility‑scale solar, $70‑$85 bn for rooftop solar, $53‑$75 bn for on‑ and offshore wind, $50‑$83 bn for storage, $75‑$100 bn for green hydrogen & ammonia, $53‑$75 bn for the EV ecosystem, $8‑$27 bn for grid T&D upgrades, and $30‑$50 bn for energy‑efficiency retrofits. The most compelling demand‑side opportunities are industrial electrification and green hydrogen (≈ $85 bn), the EV ecosystem (≈ $70 bn), and rural‑household solar under “PM Surya Ghar” (over 300 M homes, $120‑$145 bn TAM). State‑level attractiveness scores rank Rajasthan, Gujarat, Andhra Pradesh, Tamil Nadu and Karnataka highest, reflecting superior renewable resources, healthy DISCOMs, easy land access, strong policy support and robust grids.

Policy levers that de‑risk the build‑out include SIGHT 2.0 hydrogen incentives, the EU CBAM driving $85 bn of industrial decarbonisation, Production‑Linked Incentives for domestic solar‑module and battery‑cell manufacturing, FAME III EV subsidies with GST parity, round‑the‑clock (RTC) tenders that make storage bankable, and green‑hydrogen export corridors with Japan, South Korea and the EU (locking in $31.5 bn of export revenue). Key risks—DISCOM payment defaults, land‑acquisition delays, ALMM compliance, grid curtailment, critical‑mineral shortages and INR depreciation—are mitigated through escrow accounts, pre‑identified land banks, tripartite PPAs, co‑located storage, strategic mineral stockpiles and currency hedging. Expected risk‑adjusted IRRs range from 15‑20 % for export‑guaranteed hydrogen projects, 12‑15 % for utility‑scale solar PPAs and 10‑14 % for industrial electrification retrofits. The strategic playbook advises investors to lead with Gujarat and Rajasthan for large‑scale solar‑wind, anchor hydrogen and offshore wind in Andhra Pradesh, Tamil Nadu and Gujarat (leveraging port infrastructure), and take early positions in the East (Odisha, Bihar, Jharkhand) where coal‑to‑clean transitions unlock untapped demand. Achieving the 500 GW goal could shave more than $150 bn off India’s annual fossil‑fuel import bill, lift GDP growth to a 7.5 % CAGR through 2030, and cement the nation’s status as the world’s most competitive clean‑energy market.