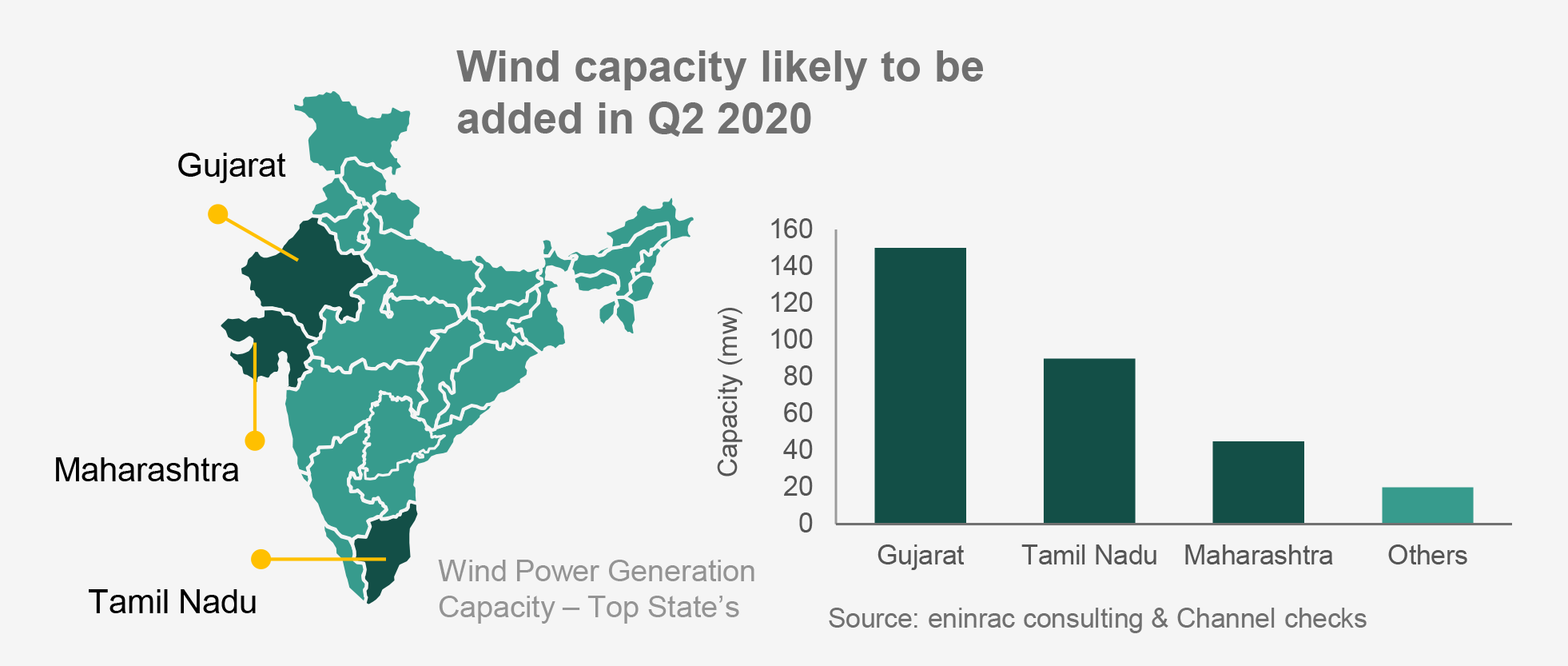

Imports of Wind turbine to India to take a massive hit in Q2 2020 due to global supply chain disruption amidst Covid-19 crisis – Cascading effect on wind projects in India expected in Q2 2020

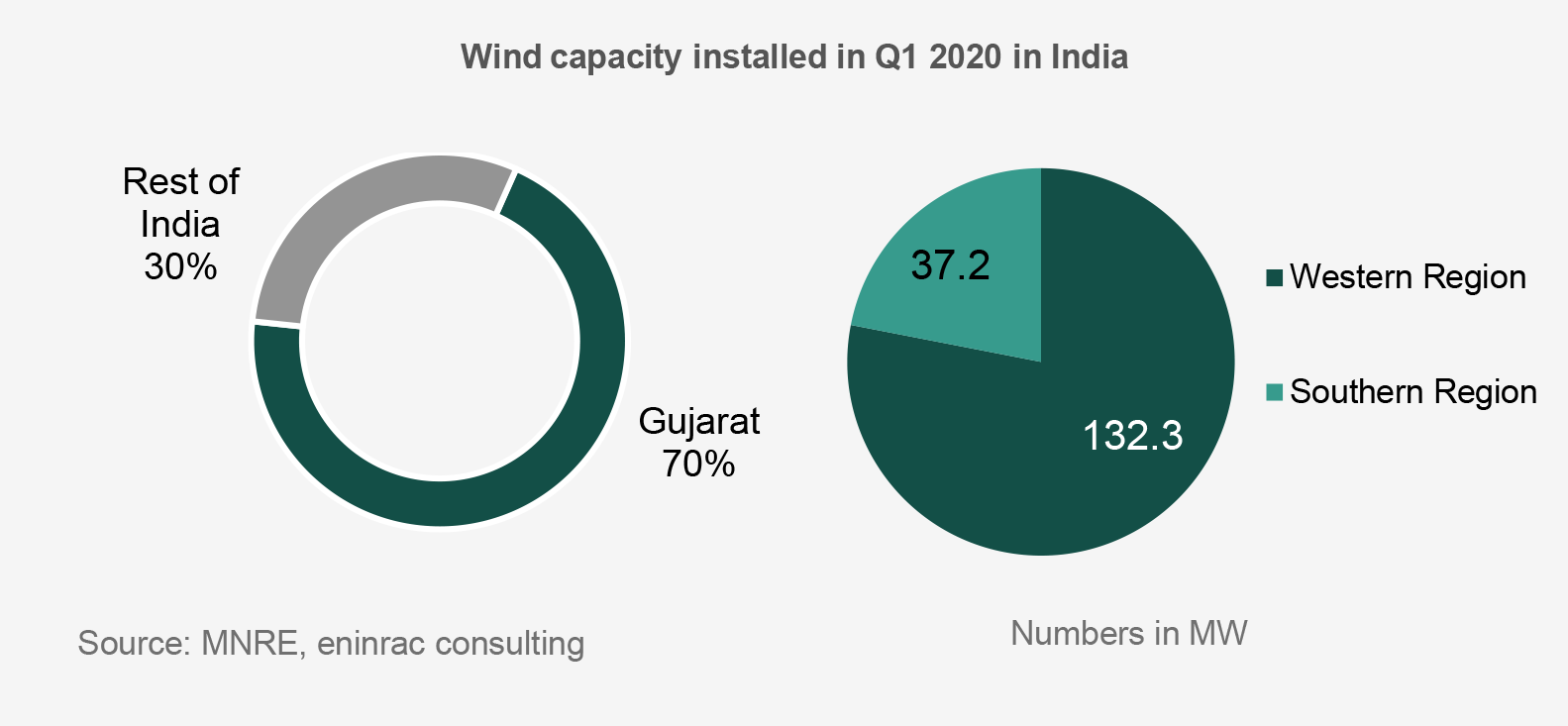

Wind installations levels in India have significantly declined after the reverse auction mechanism was introduced in the wind sector after several years of growth. Moreover, India installed only 190 MW of wind capacity in Q1 2020 which is well below the anticipated addition due to the supply chain disruptions in wind energy segment in India. Moreover, the dismal response of the wind capacity addition is mainly attributed to the financial stress of turbine makers, land acquisition issues and grid connectivity delays resulting in denting investors sentiments in wind segment. However, COVID-19 outbreak has effected the supply chains that further inflicted the wind energy segment in India. Consequently, India turbine market take a hit due to restrictions on transportation of wind turbine from China as close to 80-85% of the wind turbine are imported from China. Thus, fresh investments in the wind energy segment to take a hit in India which shall have the cascading effect on new wind energy capacity additions in Q2 2020. Moreover, as on Q2 2020, approx. 13 GW of wind energy projects in pipeline are delayed that shall dent the 60 GW target of wind capacity set by Indian Government by 2022.

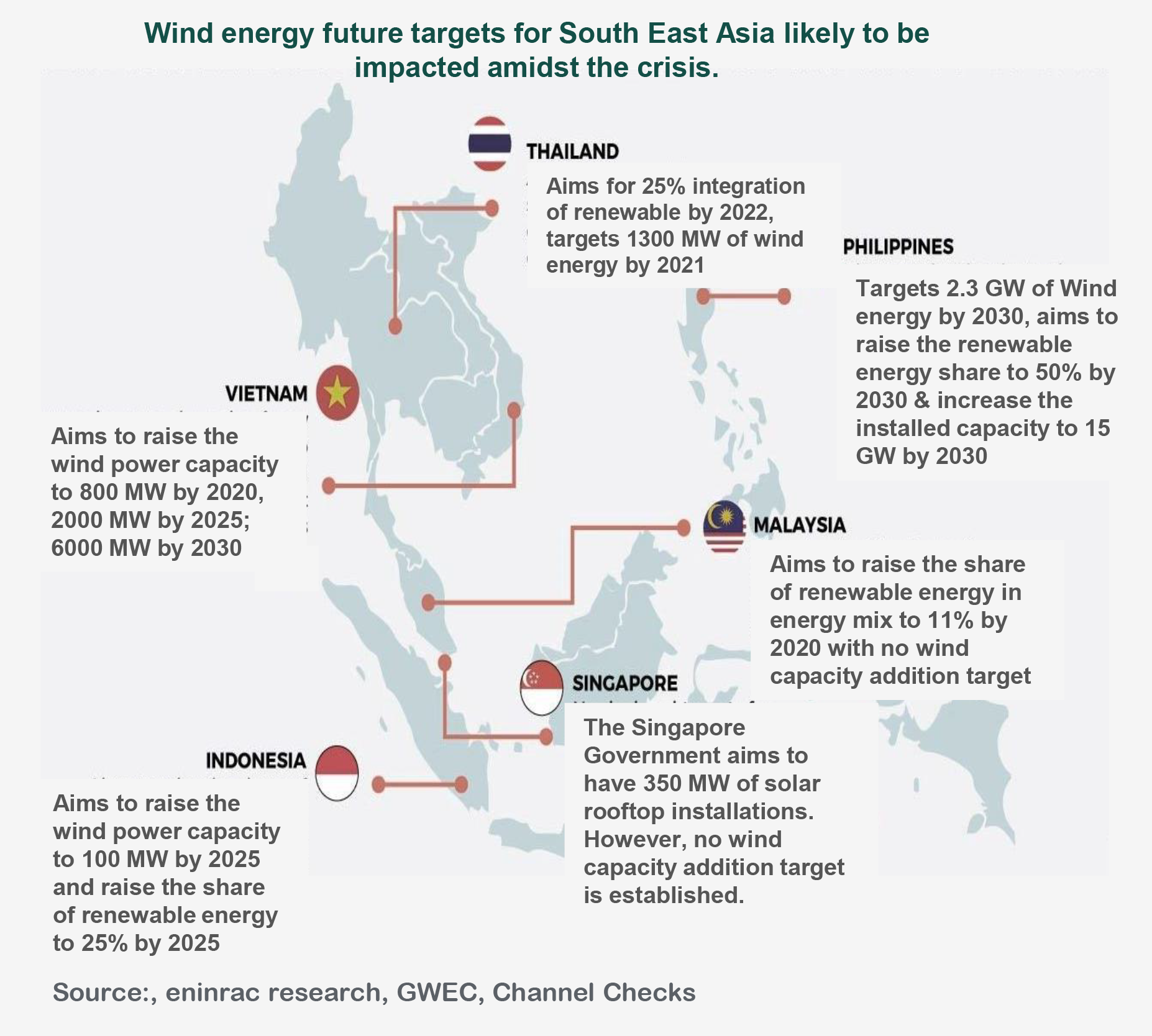

Swift transition from fossil fuel to renewable energy in South East Asia are likely to be dashed by the economic and market crises as the coronavirus outbreak persists in Q2 2020.

Southeast Asian nations already struggling to meet climate change targets will find wind capacity addition goals further from reach, with the unprecedented health emergency becoming the principal priority and a major economic burden. Although, the capacity addition has gathered pace in last two year as per year capacity addition has increased to 500MW/year which was hovering around 200 MW/year before 2018. But, the capacity addition still remains at the lower range as supportive policies are missing to give boost to capacity addition. Moreover, along with missing policy support in terms of licensing and investment in wind energy segment, the outbreak of Covid-19 has put a pause in on-going wind projects as the supply chain has been hit due to the crisis. Moreover, with no immediate relief, the future investments in the wind segment is likely to dent the future wind targets in the South East Region.