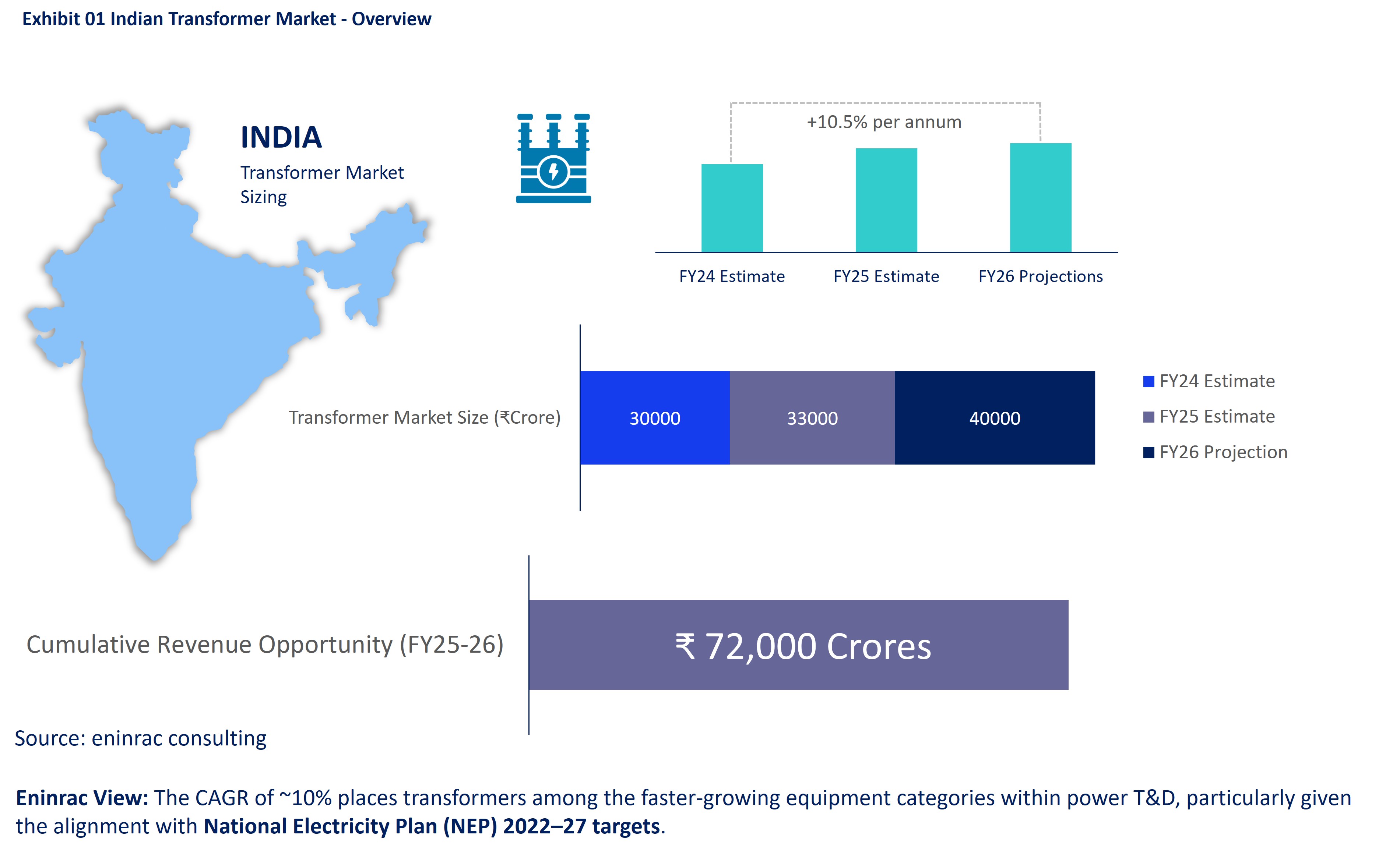

India’s transformer market will cross ₹40,000 crore by FY26, driven by rising demand, NEP targets, and replacements. A ₹75,000 crore opportunity is set to unfold over the next two fiscals.

- Chapter 1: Executive Summary

- 1.1 Market highlights (FY24–FY26 trajectory)

- 1.2 ₹40,000+ crore milestone – Key drivers and constraints

- 1.3 ₹75,000 crore cumulative opportunity window

- Chapter 2: Policy & Regulatory Landscape

- 2.1 National Electricity Plan (NEP) 2022–27 targets for T&D

- 2.2 Revamped Distribution Sector Scheme (RDSS)

- 2.3 Regulatory framework for transformer standards & localization norms

- 2.4 Deferment of transmission projects – implications for transformer demand

- Chapter 3: Market Size & Growth Outlook

- 3.1 Historical (FY20–FY24) market performance

- 3.2 Forecast (FY25–FY30) in value & volume terms

- 3.3 Transformer market segmentation (power vs. distribution transformers, ratings)

- Chapter 4: Technology Segmentation & Demand Evolution

- 4.1 Growth of HV, EHV, UHV transformers

- 4.2 Smart transformers & digital monitoring adoption

- 4.3 Oil-filled vs. dry-type transformer demand trajectory

- Chapter 5 Impact of Renewable Energy Expansion

- 5.1 500 GW RE target – grid integration challenges

- 5.2 BESS deployment & its impact on transformer sizing & deferment of lines

- 5.3 Solar/wind evacuation needs & substation transformer demand

- Chapter 6:Financial & Operational Landscape

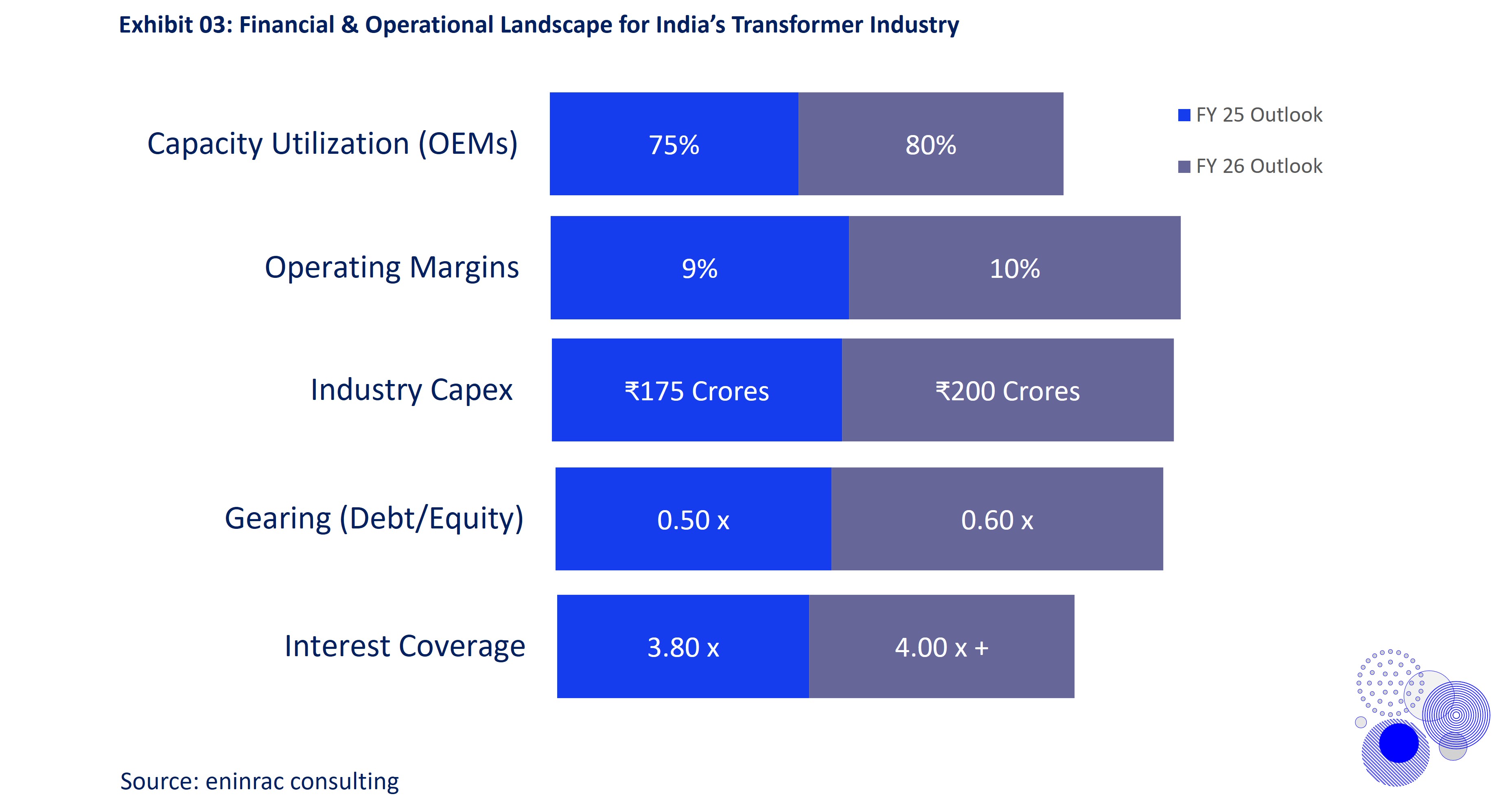

- 6.1 Industry P&L profiling (margins, gearing, utilization)

- 6.2 Capex pipeline of OEMs and new manufacturing lines

- 6.3 Working capital cycles & debt sustainability

- Chapter 7: Regional Opportunity Analysis

- 7.1 Transformer demand outlook by region (North, South, East, West, NE India)

- 7.2 Demand hotspots from RE corridors, urbanization & industrial hubs

- 7.3 Leading states with maximum opportunity (Gujarat, Maharashtra, UP, TN, Karnataka)

- Chapter 8: Utility & Discom Demand Outlook

- 8.1 State discoms – investment plans & transformer procurement

- 8.2 Central utilities (PGCIL, NTPC, NHPC)

- 8.3 IPPs & private distribution licensees

- Chapter 9: Industrial & C&I Demand Outlook

- 9.1 Transformers in Industrial Estates & SEZs

- 9.2 Demand from Metals, Cement, Petrochemicals, and Data Centers

- 9.3 Role of Make in India Push & Captive Power

- 9.4 Demand from Emerging Industrial Clusters & Smart Cities

- 9.5 Renewable Energy Integration within Industries

- Chapter 10: OEM Competitive Benchmarking

- 10.1 Market Positioning of Leading OEMs

- 10.2 Product Portfolio & Technology Capabilities

- 10.3 Manufacturing Footprint & Capacity

- 10.4 Pricing & Cost Competitiveness

- 10.5 Financial Performance & Scale

- 10.6 Strategic Partnerships & Collaborations

- Chapter 11: OEM Production & Expansion Capacity

- 11.1 Current manufacturing capacity (MVA & units per annum) by OEM

- 11.2 Expansion projects (greenfield/brownfield) planned by FY27

- 11.3 Export orientation & localization capabilities

- Chapter 12: Supply Chain & Raw Material Landscape

- 12.1 Steel, copper, aluminium availability & pricing trends

- 12.2 Import dependence & PLI opportunities

- 12.3 Logistics, tariffs & supply disruption risks

- Chapter 13: Risk & Challenge Mapping

- 13.1 Competitive pricing from Chinese OEMs vs. localization barriers

- 13.2 Margin pressures amid rising input costs

- 13.3 Financing bottlenecks for smaller OEMs

- 13.4 Technology obsolescence risk with smart grid evolution

- Chapter 14: Strategic Roadmap & Future Trends

- 14.1 Profiles of top 20 datacenter players in India

- 14.2 HVDC & UHV transmission corridors

- 14.3 Transformer role in smart grids & flexible AC transmission systems (FACTS)

- Chapter 15: Eninrac Insights & Recommendations

- 15.1 Short-term (FY25–26) actionable opportunities

- 15.2 Medium-term (FY27–30) growth levers

- 15.3 Strategic Guidance for

- OEMs (capacity, product mix, export focus)

- Utilities & discoms (procurement models)

- Investors (M&A opportunities, equity inflow pockets)

The Indian transformer market is poised to enter a decisive high-growth phase, with annual sales projected to surpass ₹40,000 crore in FY26, up from an estimated ₹33,000 crore in FY25. This translates into a healthy 10–11% year-on-year growth trajectory, underscoring the sector’s centrality to India’s evolving power ecosystem.

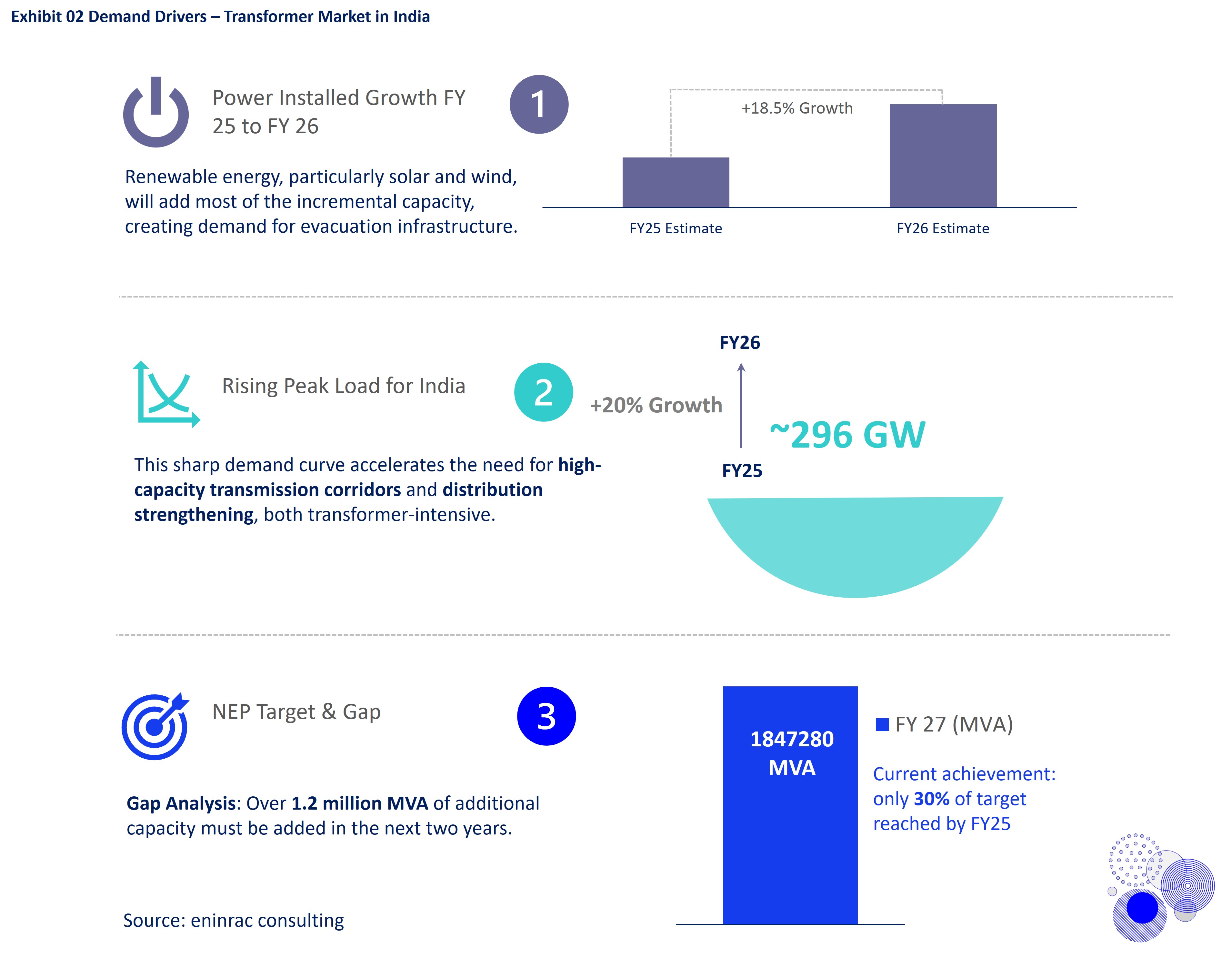

At the core of this growth are structural drivers that reinforce sustained demand for transformers across voltage classes and applications. On the supply side of electricity, India’s generation capacity is witnessing rapid expansion—led not only by conventional coal and hydro additions but also by a massive build-out of renewable energy projects, which necessitate robust evacuation infrastructure. Parallelly, accelerated transmission and distribution (T&D) investments, particularly through programs such as GatiShakti, Revamped Distribution Sector Scheme (RDSS), and state-level network augmentation, are creating significant opportunities for OEMs.

A further demand boost is expected from the replacement cycle, as a large installed base of transformers—many over two decades old—reaches the end of its economic life. This cycle is increasingly intertwined with efficiency mandates, where utilities seek to replace aging, loss-prone equipment with energy-efficient, digitally enabled transformers. Beyond the domestic market, India’s potential to emerge as a manufacturing and export hub adds another layer of opportunity, driven by competitive costs, policy support for localization, and rising global demand for grid-strengthening equipment. Taken together, these factors establish the transformer industry as a ₹40,000+ crore market opportunity by FY26, with strong prospects for both established OEMs and new entrants.

- First hand sector knowledge and inputs

- Primary research inputs from F2F interviews with domain experts

- Experts insights and market reviews taken into consideration Validated data and analysis Opportunity mapping and market sizing

- Germinates from minds that think fresh to evolve path finding guide for all stake holders through quality information and analysis

- Free query handling and analyst support for three months from the date of report procurement

- Will India’s transformer industry capitalize on rising T&D investments and renewable integration to build global competitiveness, or will challenges of scale, localization barriers, and pricing pressures restrict its growth potential?

- What are the key demand drivers fueling growth in India’s transformer market, and how are they reshaping the outlook for FY25–26 and beyond?

- How will demand translate into financial stability and operational efficiency for OEMs?

- How is the competitive landscape evolving in India’s transformer market?

- Key Signpost – How Rising Grid Investments and Replacement Demand Are Set to Transform India’s ₹40,000 Crore Transformer Market by FY26?

Resilient, Digitalized, and Grid-Ready – Next-Gen Transformers to Power India’s ₹40,000 Crore T&D Expansion by FY26

Transformers form the backbone of India’s power sector, enabling reliable, efficient, and scalable electricity transmission across the grid. As T&D networks expand and modernization accelerates, next-gen transformers with higher efficiency, digital monitoring, and enhanced durability are becoming pivotal. With rising replacement demand, grid integration needs, and technology upgrades, the transformer industry is set to play a central role in supporting India’s ₹40,000 crore power infrastructure push by FY26.

For Developers

- First-mover advantage in capacity expansion to cater to rising demand from T&D investments, renewable integration, and large-scale replacement cycles.

- Greenfield opportunities in manufacturing high-efficiency, digital, and smart transformers to align with India’s grid modernization and smart metering initiatives.

- Technology localization potential through partnerships with global OEMs for advanced materials, digital monitoring systems, and energy-efficient designs tailored to Indian grid conditions.

For Material Innovators & R&D Institutions

- Strong IP opportunity in developing advanced insulating materials, amorphous/nanocrystalline cores, high-temperature superconducting windings, and eco-friendly transformer fluids tailored for Indian grid conditions.

- Government and corporate R&D funding accessible through schemes under the Ministry of Power, DST, and collaborative programs with utilities for grid modernization and energy efficiency.

For OEMs

- Scale domestic production of advanced transformers across power, distribution, and specialty categories to meet rising T&D and renewable integration demand.

- Leverage PLI and ‘Make in India’ schemes to support local manufacturing of key transformer components such as CRGO steel, copper windings, and insulation materials.

- Import substitution potential for high-value inputs like on-load tap changers, bushings, high-grade laminations, and smart monitoring systems.

For Developers

- Design and construct India’s expanding transmission backbone by supplying high-capacity power and distribution transformers for interstate and intra-state grid projects.

- New business lines in advanced transformer systems such as digital/smart transformers, high-voltage direct current (HVDC) units, and energy-efficient designs aligned with renewable integration.

- Opportunity to build capabilities in upgrading existing grid infrastructure through retrofitting, refurbishment, and replacement of aging transformer fleets to meet modern efficiency and reliability standards.

- Power Transmission & Distribution Utilities (PGCIL, State Discoms, RE transmission developers)

- Renewable Energy Project Developers (Solar, Wind, Hybrid, RTC projects requiring evacuation infra)

- Industrial & Commercial Consumers (Steel, Cement, Data Centers, Railways, EV Charging Infra)

- Transformer OEMs & Component Manufacturers (BHEL, ABB/Hitachi, Siemens, CG Power, KEC)

- Smart Grid & Digital Solution Providers (IoT, AI-based monitoring, predictive maintenance)

- EPC Contractors (transmission, substation, and grid modernization projects)

- Raw Material Suppliers (CRGO steel, copper, insulation oils, nanocrystalline cores)

- Export Market Buyers (Africa, Middle East, Southeast Asia utilities)

- Government & Regulatory Bodies (CEA, MNRE, MoP, BIS)

- Institutional Investors & Infrastructure Funds (pension funds, sovereign funds, power-focused PE players)

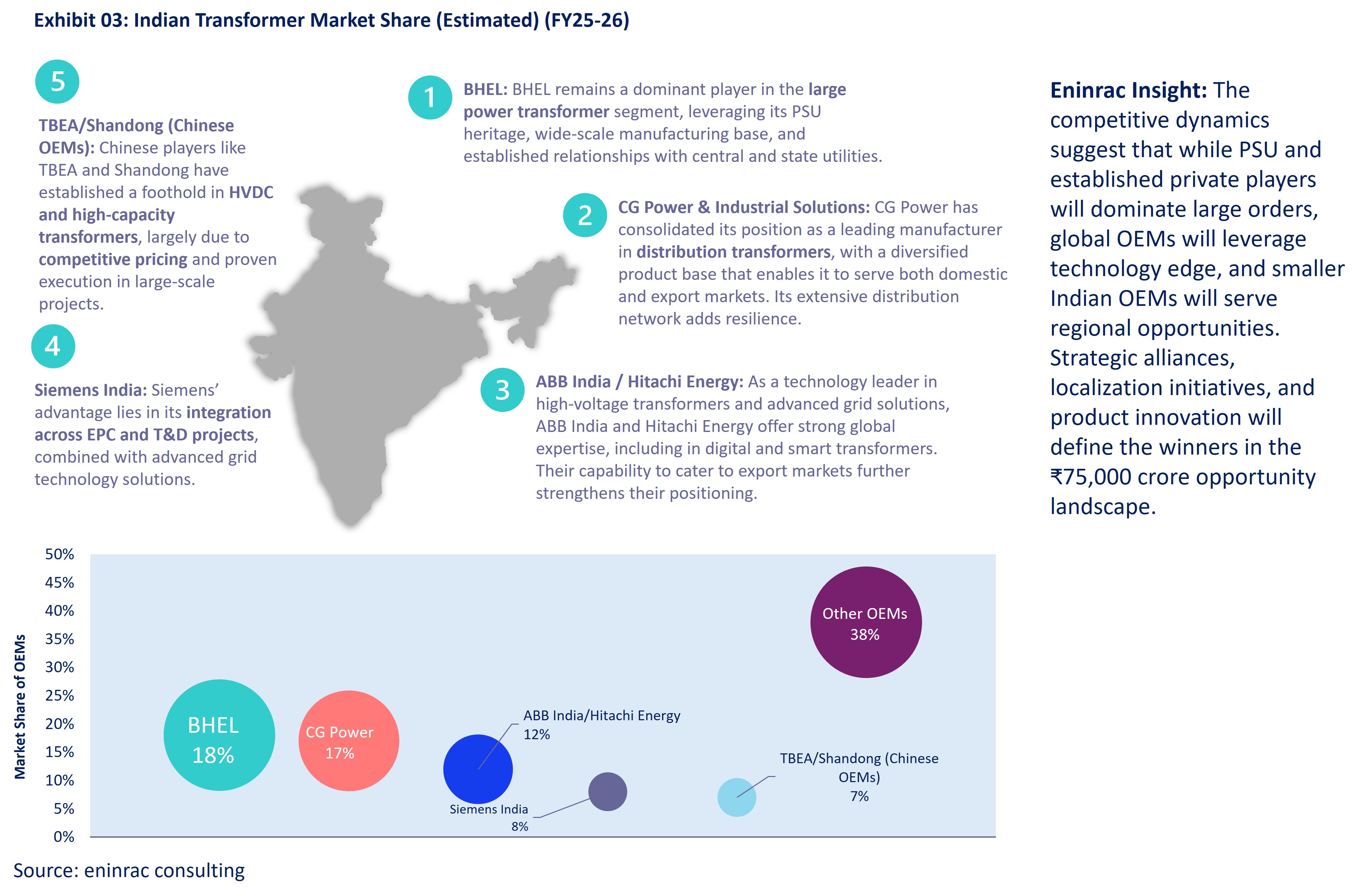

- BHEL (Bharat Heavy Electricals Ltd.)

- CG Power and Industrial Solutions Ltd.

- Siemens India

- Hitachi Energy India (formerly ABB Power Products & Systems India)

- GE T&D India Ltd.

- Schneider Electric India

- Toshiba Transmission & Distribution Systems (India) Pvt. Ltd.

- Emco Ltd.

- Kirloskar Electric Company Ltd.

- Voltamp Transformers Ltd.

- Indo Tech Transformers Ltd.

- Transformers & Rectifiers (India) Ltd.

- Diamond Power Infrastructure Ltd.

- Lakshmi Electrical Control Systems Ltd

- AT&S Transformers

- Powergear Ltd.

- Kaycee Industries Ltd.

- Jackson Power Solutions

- Easun Reyrolle Ltd.

- Best Transformers Ltd.

Q1. What is the current size of the transformer market in India?

The Indian transformer market is valued at around ₹35,000–38,000 crore in FY25, with a projected CAGR of ~8–10% driven by T&D expansion, industrial demand, and renewable integration.

Q2. What are the major growth drivers of transformer demand in India?

Key drivers include government-led grid expansion, renewable energy integration, industrial growth in SEZs and corridors, Make in India push, and modernization of aging distribution networks.

Q3. Which transformer segments are witnessing the highest demand growth?

Distribution transformers (up to 33 kV) see the highest volume demand, while power transformers (132 kV and above) drive value growth due to HVDC/UHVDC and renewable evacuation projects.

Q4. How does renewable energy impact transformer demand?

Renewables create strong demand for inverter-duty, evacuation, and step-up transformers, particularly in solar and wind parks. Hybrid projects and BESS integration further boost requirements.

Q5. Who are the leading transformer OEMs in India?

Key players include BHEL, CG Power, ABB Hitachi Energy, Siemens Energy, Toshiba, TBEA, and Bharat Bijlee, along with strong mid-size players like Voltamp, EMCO, and Shirdi Sai.

Q6. How competitive is the Indian transformer market compared to global standards?

India is cost-competitive due to lower manufacturing costs but faces challenges in high-end technology and global certifications. However, Indian OEMs are increasingly exporting to SE Asia, Africa, and the Middle East.

Q7. What role does policy and regulation play in transformer demand?

Government programs like RDSS, Green Energy Corridor, Make in India, and high-voltage transmission expansion directly boost demand. BIS standards also mandate efficiency upgrades in distribution transformers.

Q8. How are digital and smart transformers shaping the market?

Digital monitoring, IoT, and condition-based maintenance are becoming critical for utilities and data centres. Smart transformers help reduce outages, improve efficiency, and integrate with smart grids.

Q9. What are the key challenges for the transformer industry in India?

Challenges include volatility in raw material prices (CRGO steel, copper, aluminium), intense price-based competition in tenders, import dependency for core materials, and delayed payments from utilities.

Q10. What is the long-term outlook for India’s transformer market?

Strong growth is expected, crossing ₹55,000–60,000 crore by FY30, backed by renewable integration, urban infrastructure, EV charging ecosystems, and industrial expansion. Export opportunities will also rise with India positioning as a global manufacturing hub.