Why Eninrac's market research report on India’s Small Modular Reactor (SMR) segment is essential for decoding a $20Bn opportunity and identifying high-potential deployment clusters through extensive stakeholder (VoC) insights

- Executive Summary, Global SMR Market Overview & Relevance to India

- SMR Technology Landscape - Competitive Benchmarking

- India’s SMR Policy & Regulatory Readiness

- Manufacturing Opportunity in India

- OEM Opportunity Track – Foreign vs. Domestic

- Project Pipeline & Development Outlook

- State-wise Demand Mapping & Deployment Potential

- Fuel Sourcing Strategy & Nuclear Fuel Cycle Readiness

- Financing & Business Models

- Supply Chain Development –Critical Gaps

- Risk Analysis

- Competitive Landscape - Market Positioning

- Strategic Recommendations

- Future Outlook (2030–2050)

India’s path to a low-carbon, energy-secure future is increasingly tied to its ability to diversify beyond coal and integrate clean baseload options. As of 2025, Small Modular Reactors (SMRs) have emerged as a viable, scalable, and policy-aligned option to complement large reactors and intermittent renewables, serving both grid and off-grid applications.

SMRs are poised to unlock a potential $20 billion opportunity in India’s nuclear segment over the next decade. Backed by indigenous R&D, global OEM interest, and a push for industrial decarbonization, SMRs could play a transformative role in India's energy mix. Offering passive safety features, modular construction, and greater siting flexibility, SMRs are poised to fill a critical gap in India’s clean energy transition by enabling faster, decentralized nuclear deployment across industrial and remote regions.

- First hand sector knowledge and inputs

- Primary research inputs from F2F interviews with domain experts

- Experts insights and market reviews taken into consideration Validated data and analysis

- Opportunity mapping and market sizing

- Germinates from minds that think fresh to evolve path finding guide for all stake holders through quality information and analysis

- Free query handling and analyst support for three months from the date of report procurement

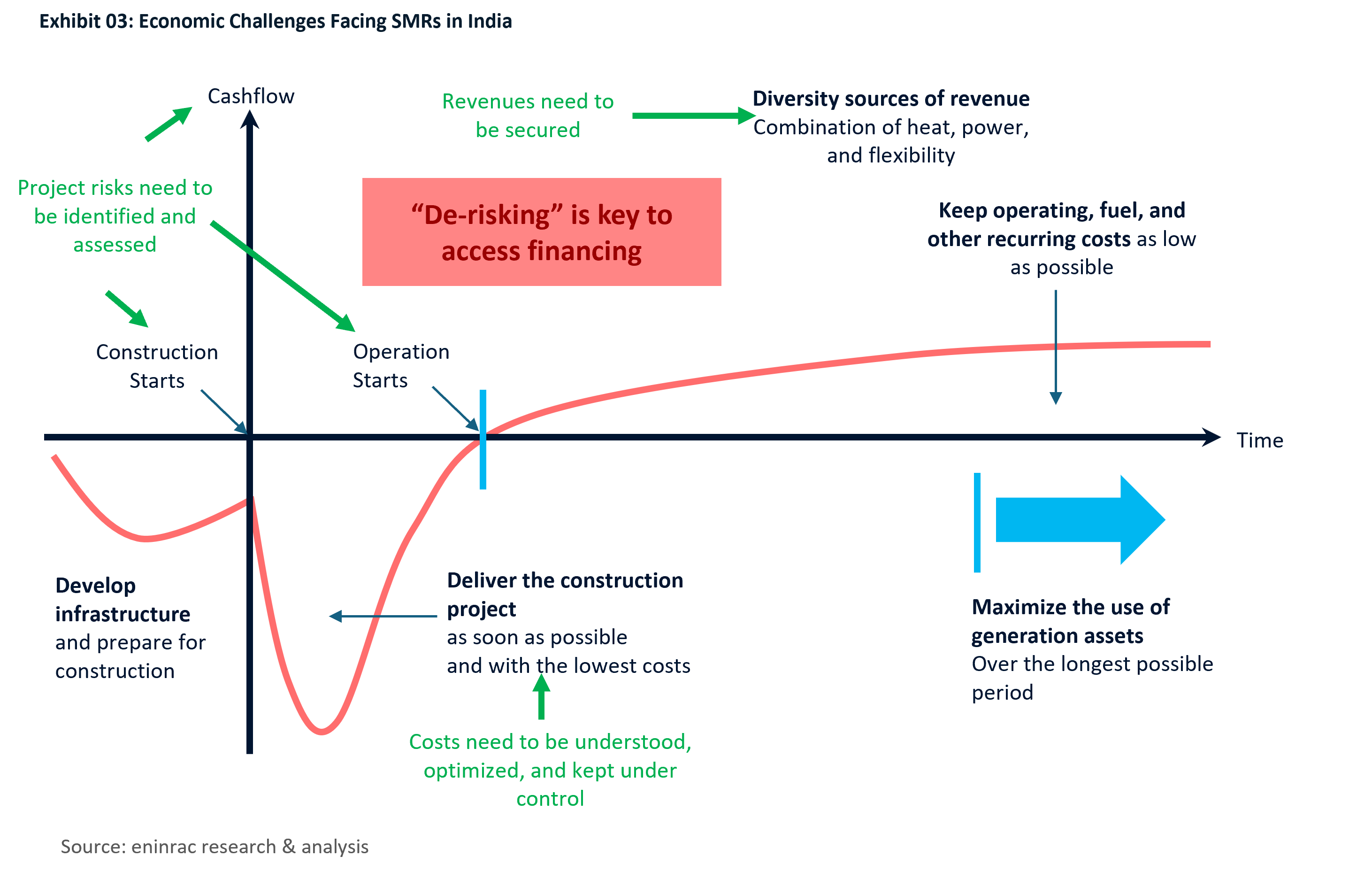

- High Upfront Capital Costs & Infrastructure Development

- Project Risk and Financing Difficulty

- Construction Phase and Cost Overruns

- Revenue Uncertainty and Market Access

- High Recurring Operating Costs

- Asset Utilization and Longevity

Small Modular Reactors (SMRs) offer the next-generation nuclear innovation that aligns with India's trilemma of energy security, net-zero targets, and industrial decarbonization. Their modularity, safety profile, and siting flexibility make them ideal for India’s growing, distributed energy demands

For Developers

- First-mover advantage in a sunrise sector with strong policy push via Make in India and potential FDI inflows.

- SMRs offer firm, clean baseload power for industrial clusters, green hydrogen hubs, and off-grid zones.

- Potential to leverage global designs and localize manufacturing, reducing long-term costs.

For OEMs

- Local manufacturing of nuclear-grade components (pumps, valves, control systems) offers new industrial capacity creation.

- Specialized opportunities in robotics, remote monitoring, passive safety systems, and digital twins.

- Long-term maintenance contracts provide annuity revenue for component and system suppliers.

For EPC Players

- Repeatable, factory-built modules enable plug-and-play deployment models, shortening construction timelines.

- High-tech, precision civil and systems integration opportunities in both greenfield and brownfield sites.

- Expertise in BOP (Balance of Plant) design, safety integration, and smart-grid interfacing will be critical

- Nuclear SMR Technology Developers

- SMR Project Developers (Public & Private)

- Independent Power Producers (IPPs)

- Large Industrial Power Consumers

- Green Hydrogen & Ammonia Producers

- EPC Companies for Nuclear Projects

- Nuclear-Grade Equipment OEMs

- SMR Module Fabricators

- Specialized Logistics & Handling Companies

- Consulting & Engineering Advisory Firms

- Government Agencies

- Regulatory Authorities

- Investment Banks & Infrastructure Investors

- Export Credit Agencies (ECAs) & Development Finance Institutions

- Climate and Energy Transition Funds

- NPCIL

- BHEL

- NTPC Ltd.

- Larsen & Toubro (L&T)

- GE-Hitachi Nuclear Energy

- NuScale Power

- Rolls-Royce SMR

- Walchandnagar Industries Ltd. (WIL)

- Godrej & Boyce

- JSW Energy

- Tata Power

- Adani Energy Solutions

- Reliance Industries Ltd.

- Indian Oil Corporation Ltd. (IOCL)

- ISRO

- Hindustan Construction Company (HCC)

- DAE (Department of Atomic Energy)

- AERB (Atomic Energy Regulatory Board)

- REC Limited

- Power Finance Corporation (PFC)

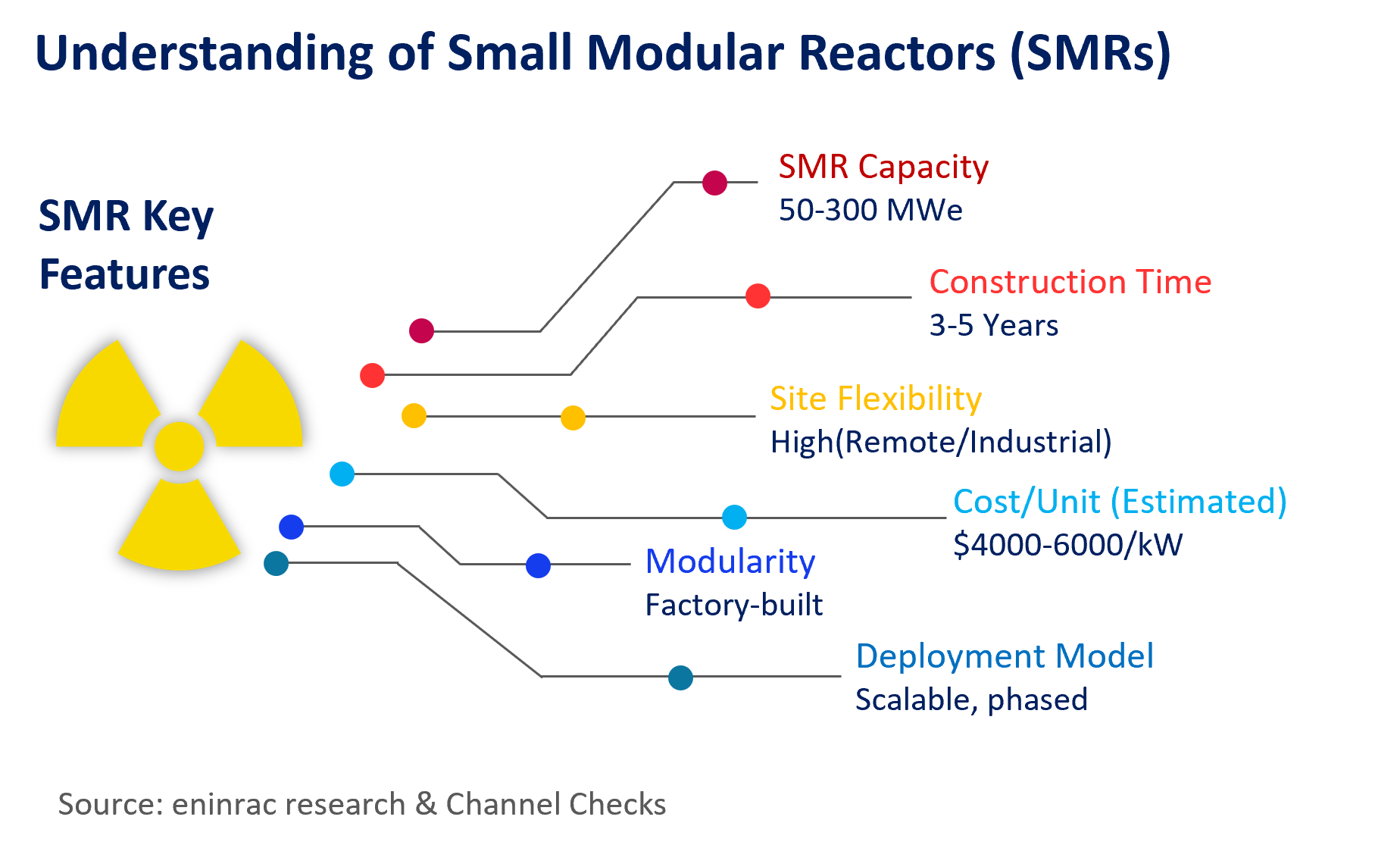

Q: What are Small Modular Reactors (SMRs) and how do they differ from traditional nuclear reactors?

A: Small Modular Reactors (SMRs) are a new class of nuclear fission reactors designed to be smaller, safer, and more scalable than traditional large nuclear power plants. Unlike conventional reactors, SMRs can be factory-fabricated, transported, and installed modularly, reducing construction time and costs.

Q: Why is India exploring SMRs as part of its energy transition?

A: India is exploring SMRs to ensure 24x7 clean base-load power, reduce carbon emissions, support industrial decarbonization, and complement intermittent renewables like solar and wind in achieving net-zero targets.

Q: Who are the key players in India SMR ecosystem?

A: Key players include NPCIL, BHEL, NTPC, L&T, GE-Hitachi, NuScale, Rolls-Royce SMR, and Walchandnagar Industries, among others. Government bodies like the DAE, AERB, and Ministry of Power also play crucial roles.

Q: Which sectors in India can benefit the most from SMR deployment?

A: Sectors such as steel, cement, data centers, fertilizers, hydrogen production, and industrial parks can greatly benefit from reliable, zero-carbon energy from SMRs, reducing dependence on fossil fuels.

Q: Are SMRs safe and economically viable in India?

A: SMRs are designed with advanced passive safety systems and smaller radioactive inventories, making them inherently safer. Economically, while initial costs are high, mass production, modular deployment, and policy support can make them viable for India's energy needs.

Q: What are the investment opportunities in India’s SMR market?

A: There are opportunities for project developers, equipment manufacturers, financiers, and green hydrogen players. Entities like PFC, REC, JBIC, and Green Climate Fund may support capital-intensive projects aligned with India’s clean energy roadmap.

Q: How do SMRs align with India’s Net Zero 2070 goal?

A: SMRs offer a carbon-free, reliable power source that complements renewable energy, making them vital for achieving India's Net Zero emissions goal by 2070, especially in hard-to-abate sectors.

Q: What is the government’s stance on SMRs in India?

A: The Department of Atomic Energy (DAE) and NITI Aayog have expressed support for SMRs as a future-ready solution for India’s growing energy demand. Regulatory processes are being streamlined to enable faster deployment.

Q: What are the challenges facing SMR deployment in India?

Key challenges include high capital costs, limited domestic technology readiness, regulatory complexity, supply chain development, and public acceptance.

Q: When can we expect the first operational SMRs in India?

A: Pilot SMR deployments are expected in the late 2020s to early 2030s, depending on regulatory approvals, international partnerships, and financial closures.