Is India cognizant enough of non-performing assets (NPAs) wave building for (RE) Renewable Energy Projects?

Is India cognizant enough of non-performing assets (NPAs) wave building for (RE) Renewable Energy Projects? Why the attribute of “prevention better than cure” not followed despite thermal power assets reeling NPAs?

Is India cognizant enough of non-performing assets (NPAs) wave building for (RE) Renewable Energy Projects?

Is India cognizant enough of non-performing assets (NPAs) wave building for (RE) Renewable Energy Projects? Why the attribute of “prevention better than cure” not followed despite thermal power assets reeling NPAs?

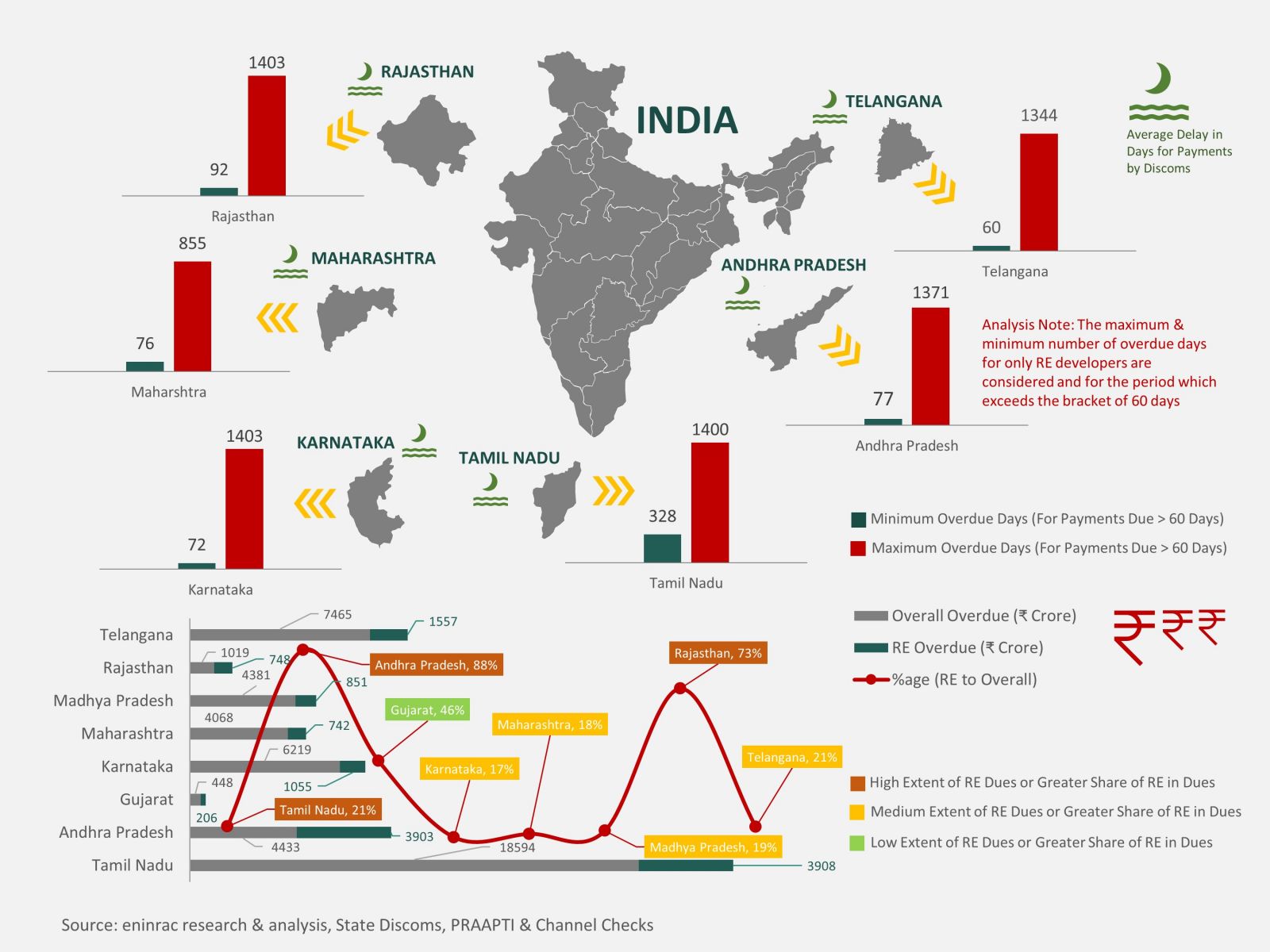

ON – POINT QUERY: Indian renewable sector has cornered bulk of private funding especially over last decade from FY10. With heavy dues piled up by discoms for RE generators, what’s the way forward for the country?

Complete the form to connect with our sales team and see the Visionboard platform in action. Discover how Eninrac helps your teams eliminate poor market research experiences and drive actionable insights.