Understanding the Asset Quality and Tracking Challenges

Stressed and Non Performing Assets Due to Non-Availability of Fuel – Status Track

Stressed and Non Performing Assets Due to Lack of PPA’s by States

Stressed and Non Performing Assets Due to Inability of the Promoter to Infuse the Equity and Working Capital

Stressed and Non Performing Assets Due to Contractual / Tariff Related Disputes

Stressed and Non Performing Assets Due to Delay in Project Implementations and Aggressive Bidding by Developers in PPA

Final Projects Rank Matrix for Investments: Eninrac’s Parametric Index

Project Tracker – In Excel Format

About

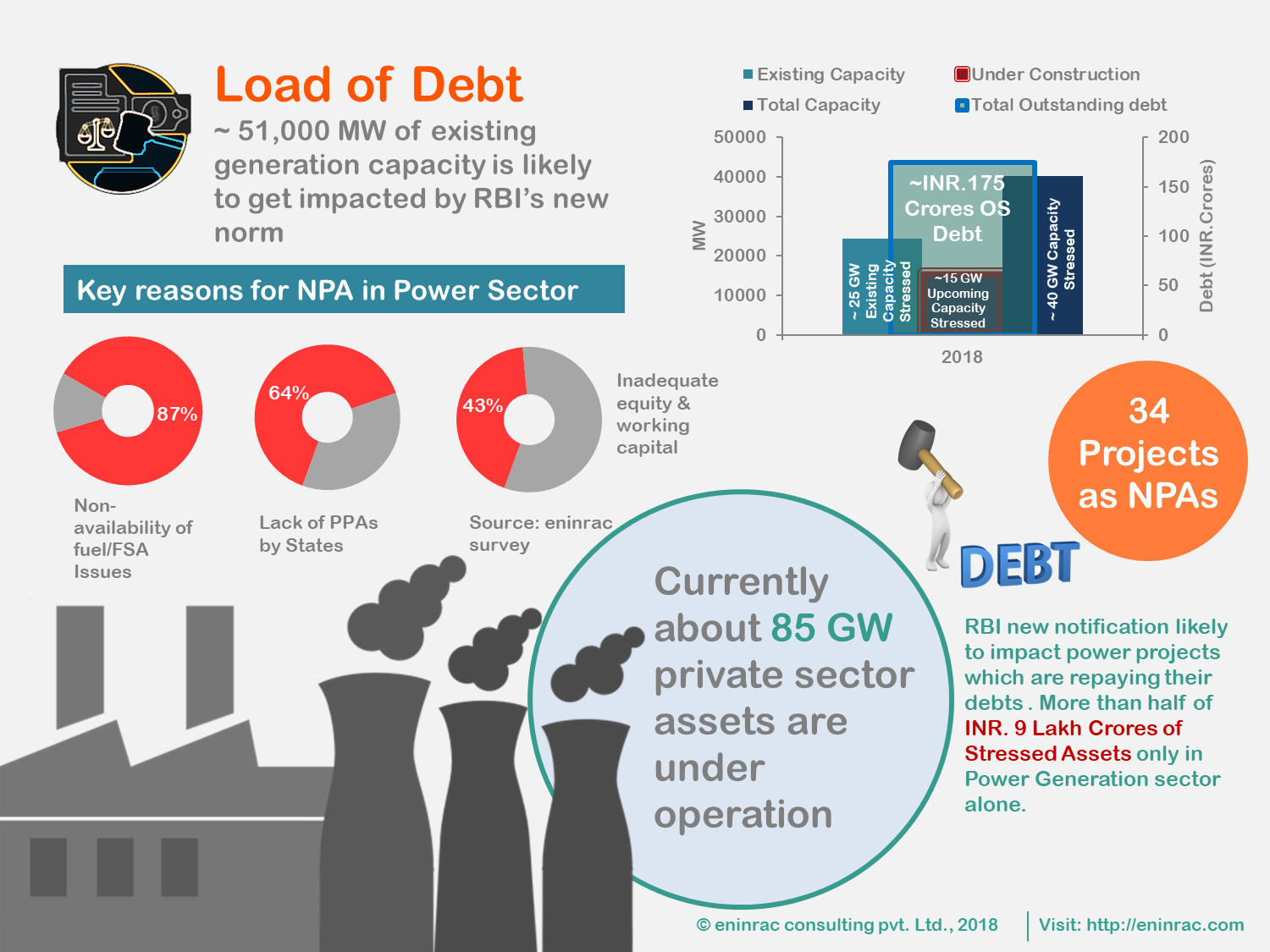

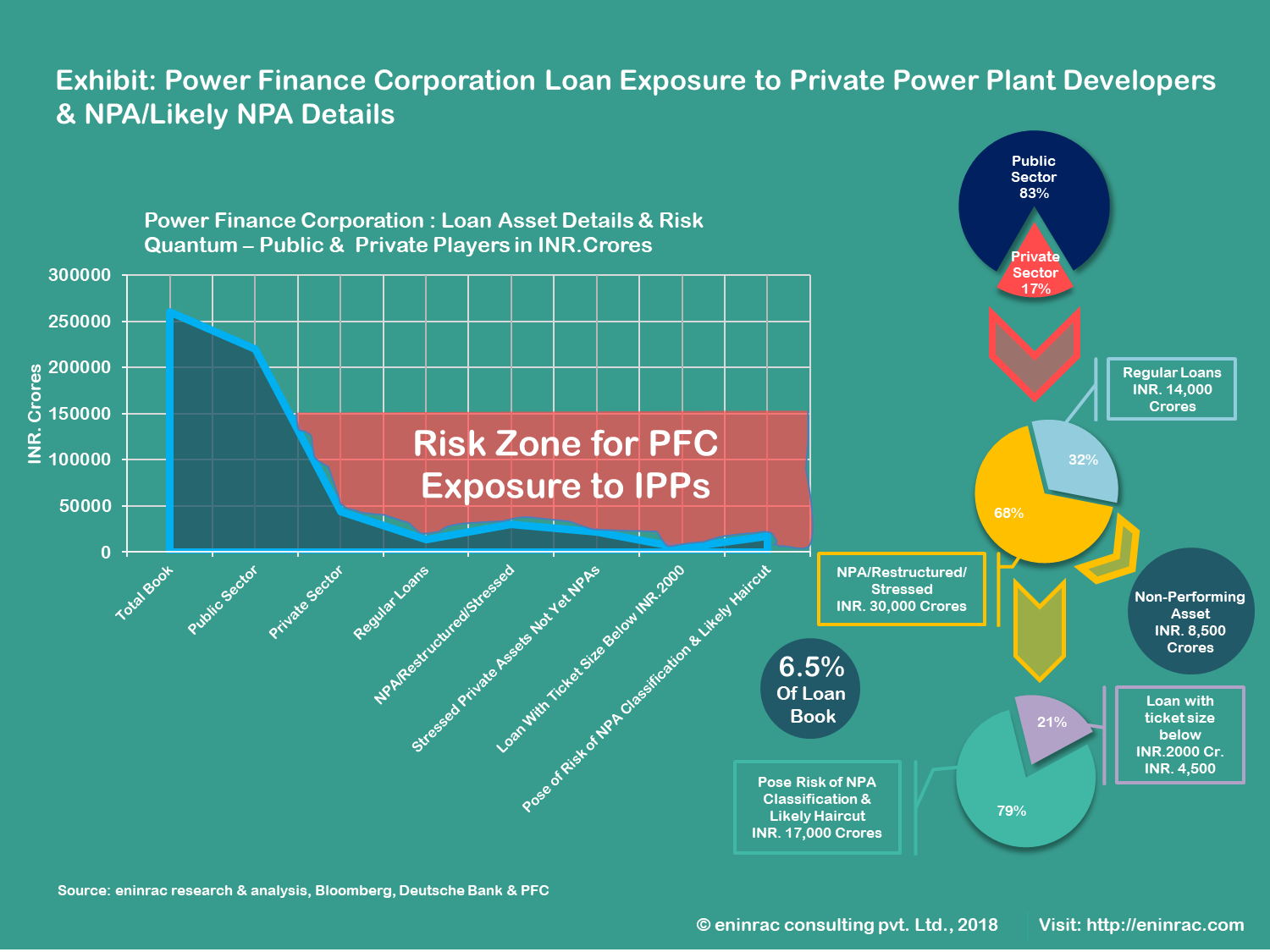

Currently, as identified by the Government 34 projects by the independent power producers do fall under the stressed category with 15 GW of upcoming and 25 GW of existing capacity are stressed. These assets are those which have slipped into to stressed assets owing to their slippage from watch list. Following such massive capacities already in the stressed category and further with new norms of RBI in place another good 50 GW of capacity is likely to be hit and demarcated under stressed assets which shall also have capacities of NTPC and SEBs.

India has seen tremendous growth rate in terms of capacity additions in thermal power capacity in the country specially post the spruced up participation by private developers. Currently the country boasts a cumulative capacity of 85 GW by independent power producers, of which most of the operators have the threat lurking on them to be pushed into NPA category. With growing burden on the IPPs close 40 GW of the 85 GW are qualified as stressed assets. The stressed assets also comprise of NPAs and those who all in likelihood may transform into one.

Key Queries Resolved

What shall be in-store for India owing to the stressed thermal power assets?

Who are the willful defaulters in thermal power plant category across different regions and states in the country?

What shall be scale of opportunity for investments in the stressed assets and good NPAs?

What are the stressed assets which are affected due to lack of fuel supply and which are the assets which may slip into NPAs due to this reason?

What are the stressed assets which are affected due to lack of PPA’s and which are the assets which may slip into NPAs due to this reason?

What are the stressed assets which are affected due to inadequate equity capital and which are the assets which may slip into NPAs due to this reason?

What are the stressed assets which are affected due to contractual/tariff related issues and which are the assets which may slip into NPAs due to this reason?

What are the stressed assets which are affected due to project implementation and aggressive bidding by developers and which are the assets which may slip into NPAs due to this reason?

How the financial & operational viability for the NPAs to be assessed to ascertain investment drive or M&A drive in them?

BUSINESS CASE FOR INVESTMENT OPPORTUNITIES IN STRESSED AND NON-PERFORMING THERMAL POWER ASSETS

With new RBI norms in place close to 51 GW of fresh capacity may become stressed and slip into NPAs presenting huge opportunity for companies like NTPC & Tata Power to articulate strategic acquisition in the country

Currently 25 GW of thermal plants are under NPA category and another 15 GW under stressed category and among this cumulative capacity scores of good assets are present which need in-depth due diligence for robust investments

Given the assimilation of stressed assets across the country chance of bankers and lenders going for a debt restructuring is certain and that opens entire market for FDI as power generation business is open for 100% of it

For the assets of SEBs which may slip under the NPA category from the stressed one’s owing to lack of equity capital or operation management issues there exists an opportunity to bail out and sell off their assets to the effective owner with affecting PPAs

For the IPPs which are struggling with issues of FSA and PPAs from the discom’s it shall be best opportunity for such players to have recovery of their assets or simply exit through by engaging in profitable M&A drive

USPS

First hand sector knowledge and inputs

Primary research inputs from F2F interviews with domain experts

Experts insights and market reviews taken into consideration

Validated data and analysis

Opportunity mapping and market sizing

Germinates from minds that think fresh to evolve path finding guide for all stake holders through quality information and analysis

Free query handling and analyst support for three months from the date of report procurement

Key Highlights

Thermal power generation round-up in India with details basis region, developer & technology of generation involved in India

Comprehensive business case evaluation of thermal power plants in India with drivers, increasing renewable portfolio, PPA issues & challenges etc.

Opportunity Sizing for investors, developers and FIIs/Bank to invest in stressed assets to increase their valuation before engaging in M&A activity

Financial Attractiveness Index for NPA’s and stressed assets basis region, state’s and owner basis which were on path of recovery owing to increased power demand cycles in India

Analysis of willful defaulters engaged in thermal power generation basis on state, region and bank wise outstanding amount to filter out assets for quarantine

Analyzing the asset quality with comprehensive due diligence of select filtered assets to indicate their attractiveness in terms of re-investments or practicing an exit option from the business

Holistic analysis of stressed assets and the watch list assets which might slip into stressed category owing to RBI norms on fuel availability issues

Holistic analysis of stressed assets and the watch list assets which might slip into stressed category owing to RBI norms on lack of PPAs with discoms

Holistic analysis of stressed assets and the watch list assets which might slip into stressed category owing to RBI norms on equity capital lack, contractual/tariff delays or aggressive bidding by the developers etc.

Eninrac’s recommendation for filtered assets vis-à-vis the time bound horizon which shall clearly be useful for strategic consultants, credit rating agencies and ARCs as well.

Report Insights

Identification of right market strategy for engaging in M&A drive for the stressed assets/NPA

Detailed examination of reasons for incidence of non-performing assets basis both internal & external factors

Holistic comparison of India with Global majors in terms of running NPAs and likelihood of projects slipping into them

Financial Attractive Indexation for TPPs in India through business case identification in current power generation mix of the country

Comprehensive track of stressed thermal power assets on basis of region & developer involving private, central & SEB track separately with the inflection analysis for new RBI norms

Tracker for willful defaulter’s in thermal power generation business with split of region, bank & state wise split compounded with loan amount details to be serviced

Detailed and robust analysis to judge the assets quality through parametric attractiveness index enabling M&A drive of asset sale

Complete market sizing of good assets, loss assets and the one’s which may have the tendency to be marked as NPAs from the watch list basis detailed due diligence from eninrac’s expert team

Profiles and detailed track of state, developer & region wise track of NPAs/Stressed assets due to unavailability of fuel

Profiles and detailed track of state, developer & region wise track of NPAs/Stressed assets due to lack of PPAs with respective discoms

Profiles and detailed track of state, developer & region wise track of NPAs/Stressed assets due to inability of promoter to infuse equity and working capital

Profiles and detailed track of state, developer & region wise track of NPAs/Stressed assets due to contractual or tariff issues

Complete the form to connect with our sales team and see the Visionboard platform in action. Discover how Eninrac helps your teams eliminate poor market research experiences and drive actionable insights.