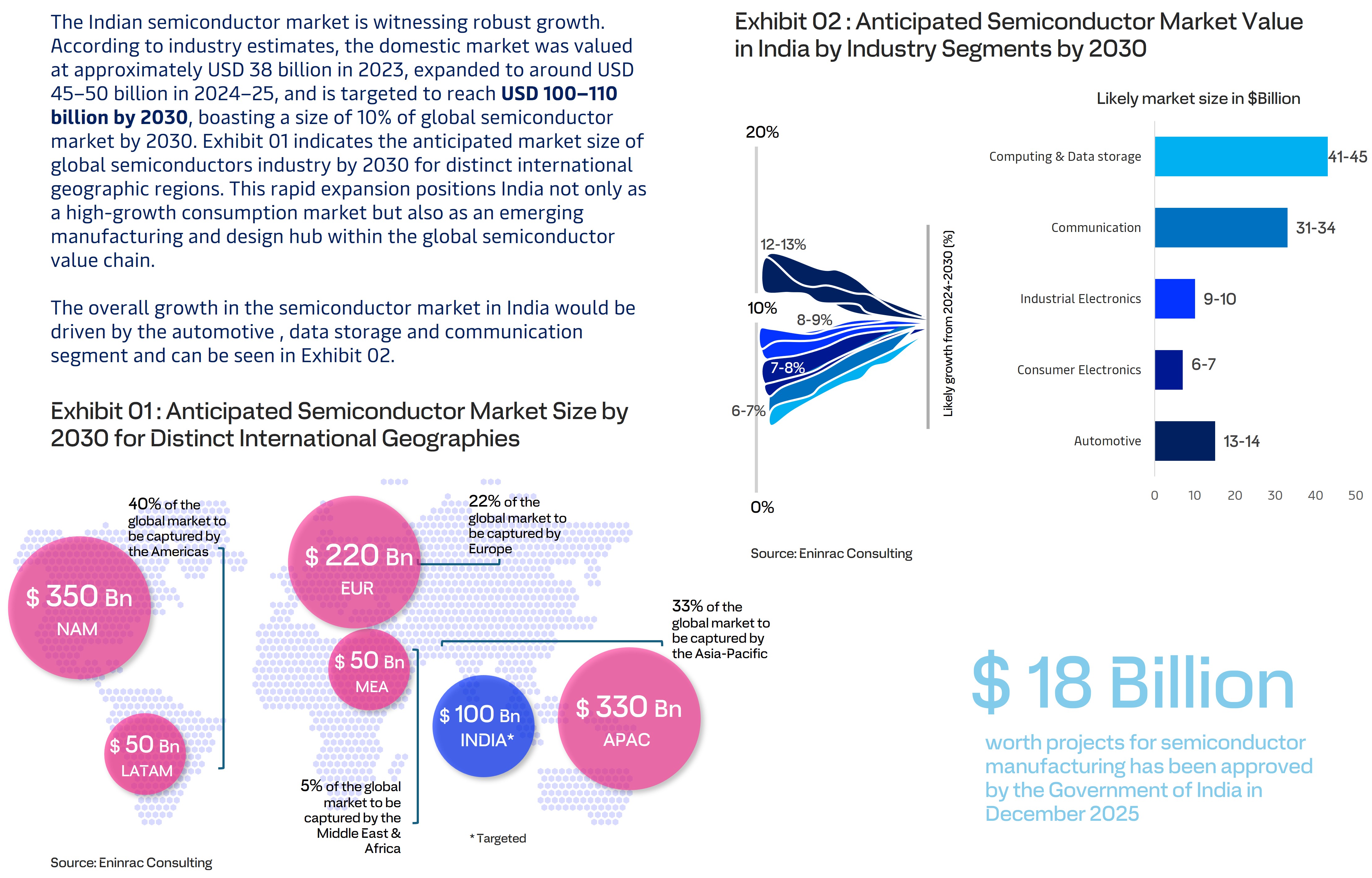

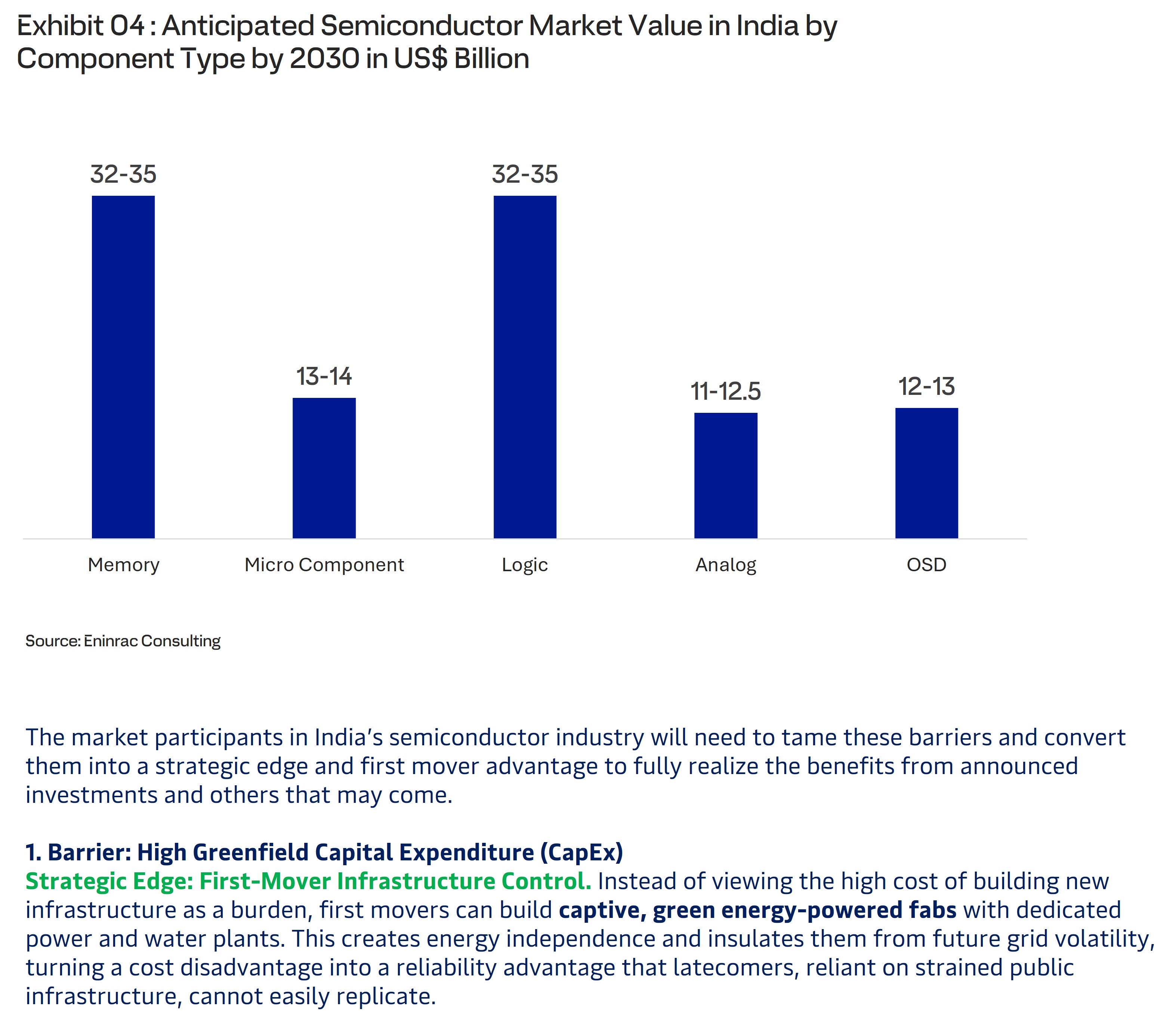

India’s semiconductor industry is poised to leap from $38 bn in 2023

to $100‑110 bn by 2030, covering roughly 10 % of the global market. By

2029, 70‑75 % of domestic chip demand—led by automotive, data‑storage

and communications—is expected to be met locally, delivering 13‑14 %

annual growth.

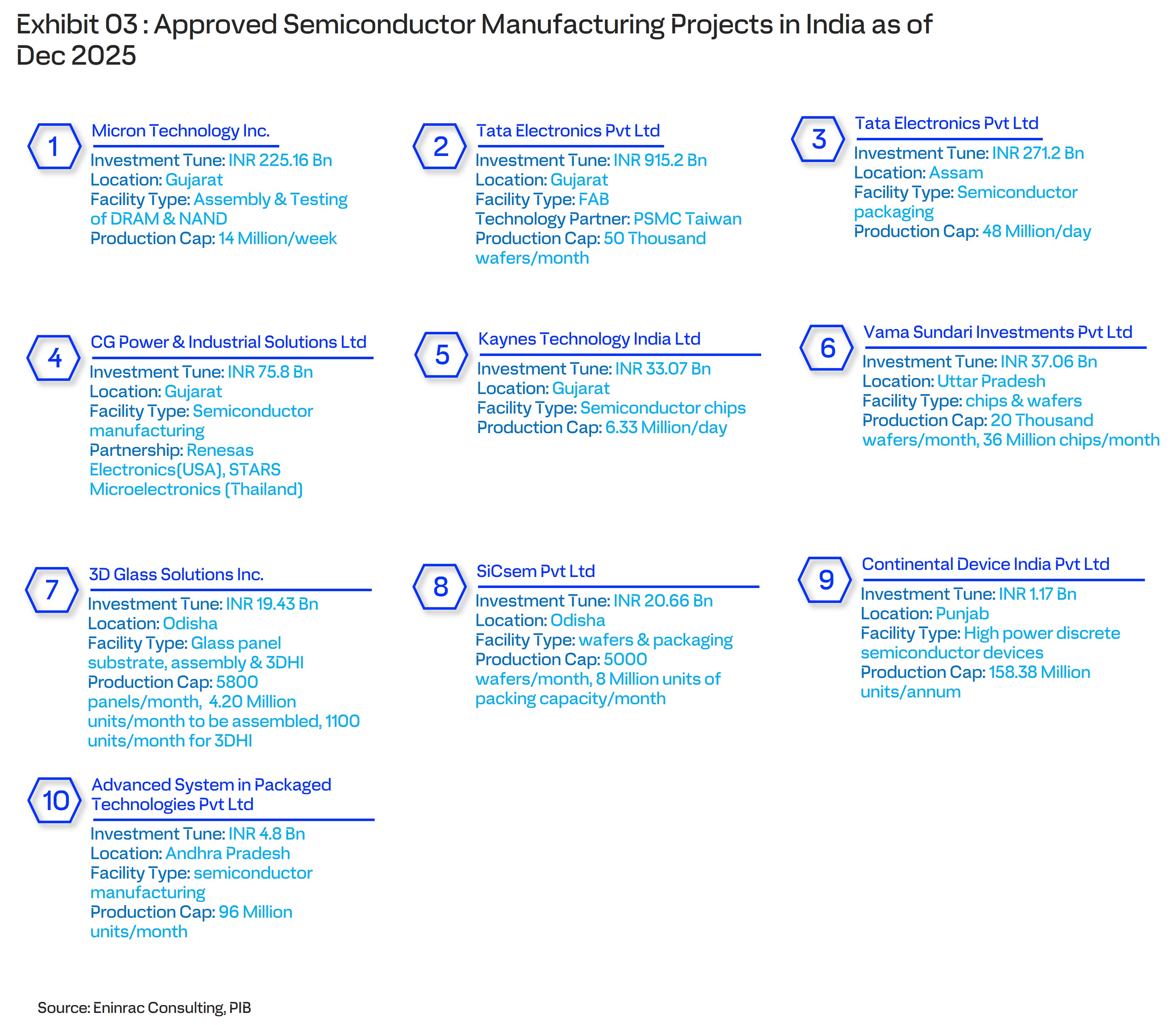

Key Government‑Backed Projects ($18 bn total)

- Gujarat: Micron DRAM line (14 M dies/week) & Tata fab (50 k wafers/month)

- Assam, Uttar Pradesh, Odisha, Punjab: assembly, testing, packaging and glass‑substrate plants

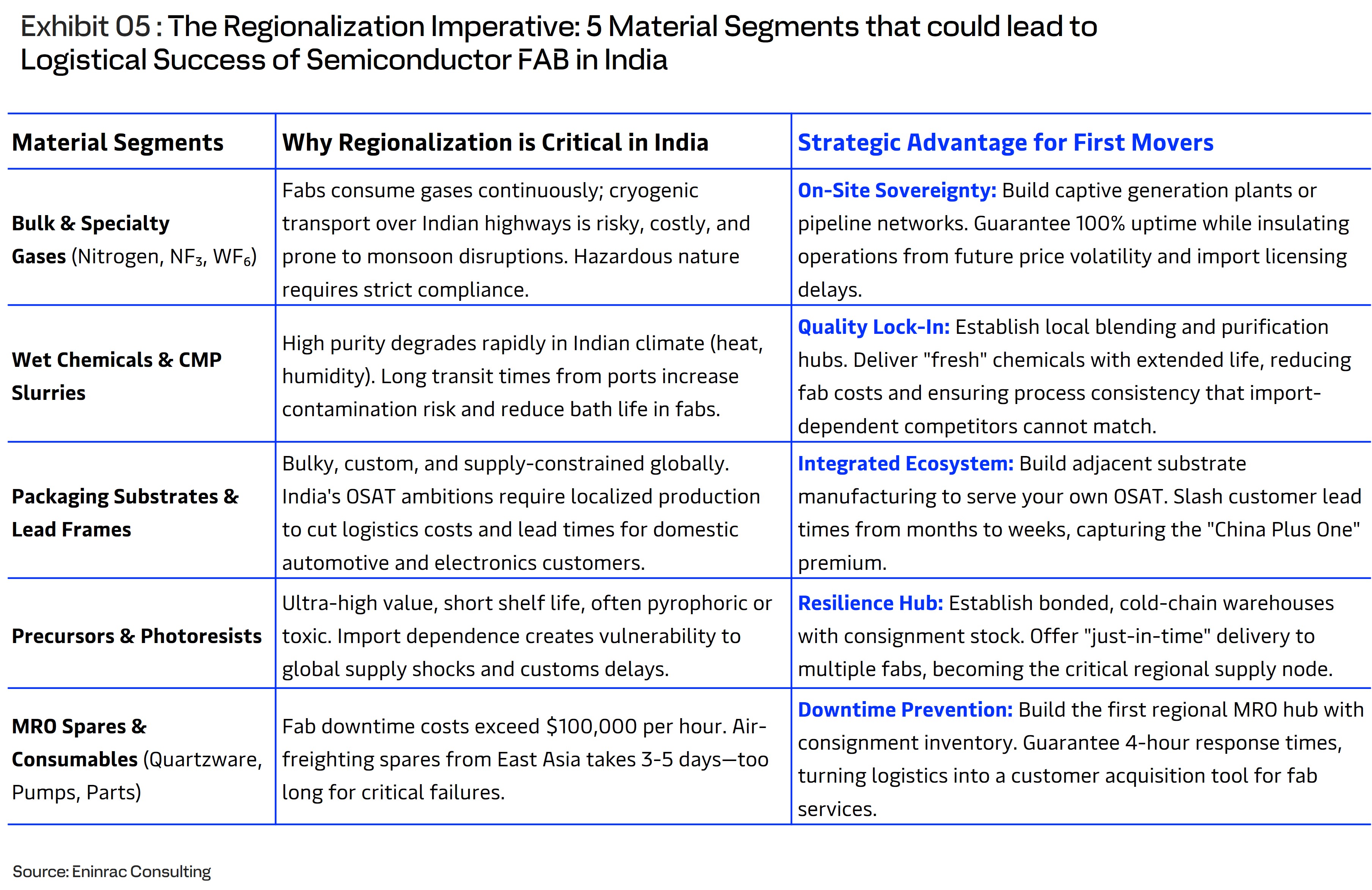

First‑Mover Moats

Captive renewable‑powered fabs to tame high CapEx & energy volatilityIndustry‑led training academies to solve the fab‑ready talent gapCo‑located specialty‑gas and quartz plants for raw‑material self‑sufficiencyIntegrated OSAT‑plus‑substrate hubs to beat East‑Asia packaging lead timesVibration‑controlled logistics terminals and inventory‑as‑a‑service for sparesDigital‑twin supply‑chain intel to pre‑empt geopolitical or climate shocks

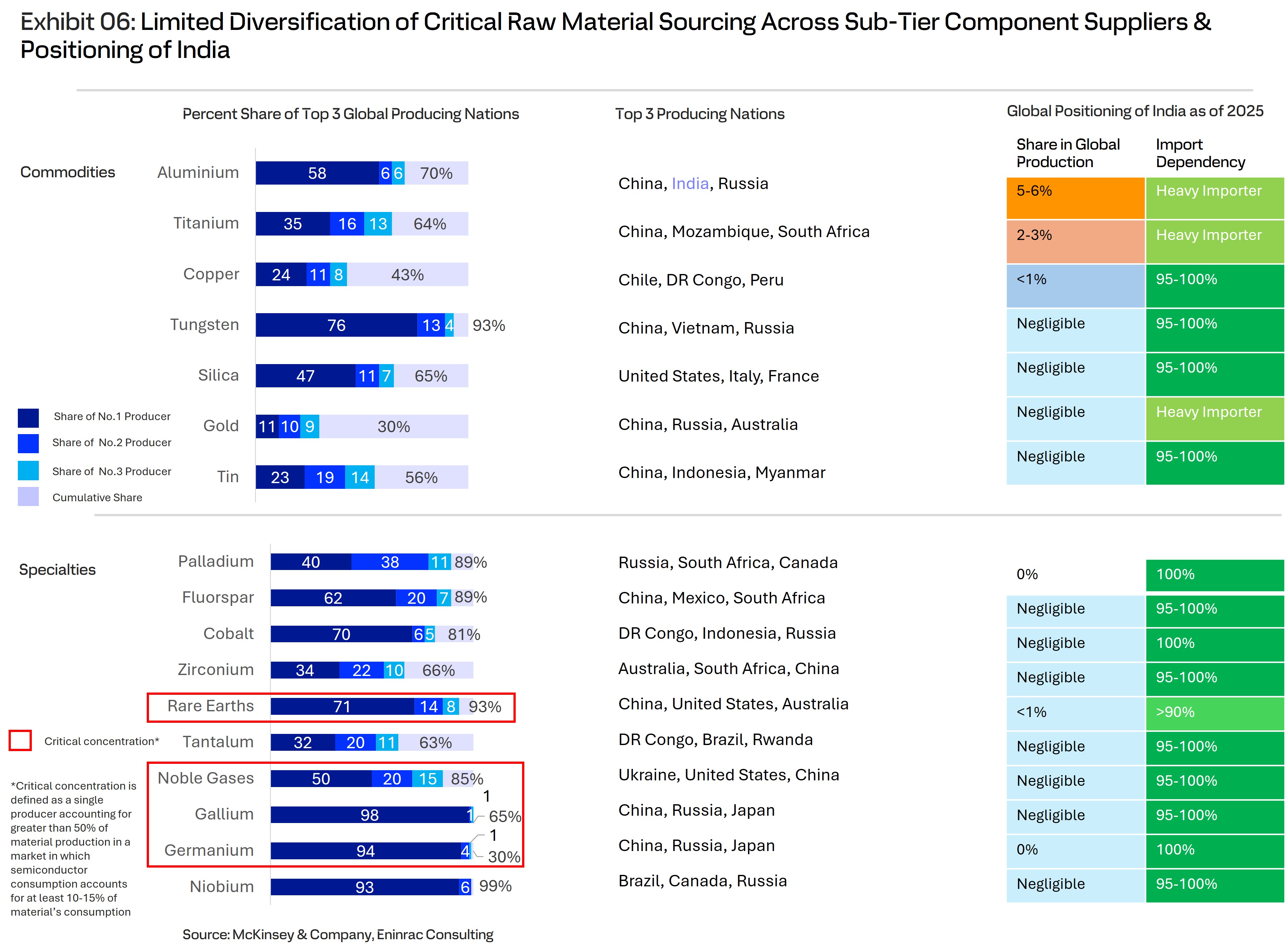

Raw‑Material Edge

India

holds abundant quartzite, ~6 % of global rare‑earths, major copper,

emerging argon/helium air‑separation, and extractable

gallium/indium—enabling upstream cost advantages and reduced import

reliance.

State‑Level Fitment

Prioritize regions with

surplus power, water, seismic stability and logistics connectivity

Gujarat (green‑energy surplus) and Odisha (port access) are top

candidates. Early engagement with state incentives can lock in a durable

geographic moat. Investors who act now can capture a $100‑bn growth

wave while shaping the future of India’s semiconductor ecosystem.