Fact Factor

Fact Factor

Report Summary Following the easing of restrictions on the wind turbine supply chain across Europe in Q3 2020, the outlook for the wind sector will depend on the effectiveness of national and EU recovery plans

European Wind Turbine Market Outlook Update Q3 2020

Share Report

License Type

In addition to single user license

- About

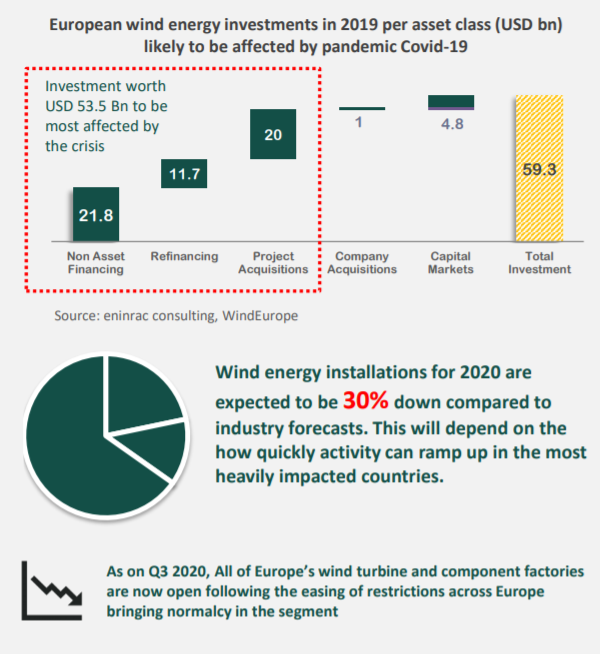

Following the easing of restrictions on wind turbine supply chain across Europe in Q3 2020, the outlook for the wind sector will depend on the effectiveness of national and EU recovery plansThe European wind industry is the global leader in the wind turbine market, realising projects in more than 80 countries worldwide. As such, its companies rely on both European and global supply chains for raw materials and components. However, outbreak of Covid-19 posed a risk to investments made in wind energy segment in Europe facing higher risk of delay or even cancellation. In 2019 the wind energy industry invested USD 59.3 bn in Europe, USD 21 bn of which was for the financing of new wind energy projects which are likely to be affected due to the crisis. Additionally, the uncertainty over the evolution of the COVID-19 crisis will also likely increase the cost of finance as banks will be less willing to lend as they are concerned about liquidity and corporate finance. In contrary, many European countries like Germany, Netherlands, Lithuania and Greece have confirmed they will stick exactly to their 2020 auction schedules. Also, France and Germany are setting out the Recovery Plan, made climate policy commitments such as: support for a higher 2030 emissions reduction target which shall put the wind turbine segment in Europe on track to bring in efficiency in supply chain.

- TOC

- USPs

- Key Highlights

- Report Insights

- Must Buy For

- Companies Mentioned

Get your report flyer

Download the flyer to learn more about:

- Report structure

- Select definitions

- Scope of research

- Companies included

- Additional data points